The governing board of a unit of local government must identify and obtain sufficient revenue to cover the costs of the services it provides. Although the services that a given North Carolina county or municipality chooses to offer can vary between jurisdictions, all county and municipal officials must understand how to legally finance the services in which their unit engages.

North Carolina law requires counties and municipalities1 to provide for and fund, in whole or in part, certain activities. Although municipalities must provide only one service—building code enforcement—counties must fund a wide variety of services, including public education, social service programs, mental health programs, emergency medical services (EMS), courts, jail facilities, and building code enforcement. Counties and municipalities also have legal authority to provide a range of other services that include, among other things, zoning and land use planning, water and sewer utility services, recreation and cultural activities, and economic development. With a few notable exceptions, counties and municipalities legally may provide, and fund, most of the same discretionary services.

North Carolina’s counties and municipalities may only impose taxes and fees when the General Assembly gives them such authority. At present, the major sources of revenue available to counties and municipalities are (1) locally imposed taxes; (2) locally imposed user fees, assessments, and charges; and (3) taxes and charges imposed by the state but shared in part with each type of local government.

A local government’s choice of revenue mechanism has legal implications, including whom and what the unit can legally tax or charge, and what procedures the unit must follow to impose the tax or fee. For example, if a county or municipality chooses to fund its services through the imposition of a property (ad valorem) tax, then property owned by government and nonprofit organizations (e.g., religious organizations, state agencies, public and private educational institutions, and federal facilities) in the jurisdiction will be exempt from taxation. In addition, North Carolina law may restrict the rate of tax that a unit charges and, under certain circumstances, require a unit to obtain voter approval to levy a tax. Conversely, a unit employing a user fee to fund a service, in part or in whole, typically only requires that those availing themselves of the service pay. In such a case, a unit’s rate structure must be reasonable and bear some relationship to the service provided to each user.

Appendix 4.1, “Local Revenue Authority and Limitations,” outlines the major revenue sources available to North Carolina’s counties and municipalities. It specifies (1) whether the source of revenue is available to counties, municipalities, or both types of units; (2) whether the General Assembly has authorized the imposition of the tax, fee, charge, or assessment through general law or local act; and (3) any restrictions on the use of proceeds. The remainder of this chapter describes each revenue source in more detail.

Local Taxes

Taxes are compulsory charges that governments levy upon individuals, entities (e.g., corporations), or property.2 In general, the amount or character of a tax need not bear any relationship to the benefit that a taxing government provides to a taxpayer.3

A unit of local government may levy a tax only with legislative authorization—via general law or local act—from the General Assembly. The legislature has authorized counties and municipalities to levy a range of taxes. The majority of county and municipal revenues in North Carolina consist of two types of taxes: property (ad valorem) taxes and local sales and use taxes. Both counties and municipalities may levy property taxes; only counties may levy local sales and use taxes, but by law, municipalities are entitled to a share of the proceeds of most of these taxes. This section details property taxes, local sales and use taxes, and other taxes that North Carolina’s local governments may levy.

The Property (Ad Valorem) Tax

The property tax is levied against real and personal property within the jurisdiction of a unit of local government. It attaches to property—not just to the property owner. The following sections describe the property tax in more detail.

Property Tax Base

A “tax base” consists of assets that a governmental entity may tax. The tax base for local property taxation in North Carolina consists of real property (e.g., land, buildings, and other improvements to land); personal property (e.g., business equipment and automobiles); and the property of public service companies (e.g., electric power companies, telephone companies, railroads, airlines, and certain other companies) that is not exempt or excluded from taxation.4

Certain types of property are exempt from taxation. For example, the North Carolina Constitution exempts government-owned property from taxation.5 In addition, the General Assembly may, on a generally applicable statewide basis, exempt certain property from taxation or classify property to exclude it from taxation, reduce its valuation, or subject it to a reduced tax rate.6 A local government may not exempt, classify, or otherwise give a tax preference to property within its jurisdiction.

Tax Rate Limitations and Voter Approval

North Carolina law does not require a county or municipality to always levy a property tax. Instead, the governing board of each municipality and county must determine whether to levy a property tax each year and, if it chooses to levy a property tax, the applicable rate or rates of taxation.

A governing board may adopt a single tax rate and use the revenue generated from the tax to fund a variety of services. Alternatively, a board may adopt a series of tax rates and earmark the proceeds for specific services.7 A governing board also may adopt a combination of these two methods. For example, a county’s governing board might establish a combined rate of property tax for most of its programs and services but a separate rate for public schools, libraries, or fire services.

Property taxes are subject to statutory rate limitations and, in a few cases, must be approved by the voters. In particular, the North Carolina Constitution prohibits the General Assembly from authorizing any “unit of local government to levy taxes on property except for purposes authorized by general law uniformly applicable throughout the State, unless the tax is approved by a majority of the qualified voters of the unit who vote thereon.”8 In other words, a local government must obtain voter approval to levy a property tax unless the General Assembly has authorized all units across the state to levy property taxes for a particular purpose.

Under these statutes, a unit’s combined rates of property tax generally may not exceed $1.50 per $100.00 of assessed valuation.9 Counties and municipalities may levy some property taxes without limitation on the rate or amount.10 For example, a municipality may levy taxes without any rate restriction to fund debt service on its general obligation debt.11 Counties may levy property taxes without any rate restriction to finance many of the services that they legally must provide: court operations and facilities, schools, social services, courts, jails, and elections.12

A county or municipality may seek voter approval to use property tax proceeds to fund an activity not specified in G.S. 153A-149 or 160A-209 but which the respective unit has statutory authority to undertake.13 It also may seek voter approval to increase a county’s or municipality’s overall property tax rate cap above $1.50 per $100.00 of assessed valuation.14

Tax Levy Formula

Governing boards of counties and municipalities must adopt a balanced budget for each fiscal year, whereby the sum of estimated net revenues and appropriated fund balance is equal to the appropriations in each fund.15 If a unit’s estimated revenues from sources other than the property tax plus appropriated fund balance will not equal the appropriations in each fund, a county or municipality must levy a property tax at a rate sufficient to balance the budget.16

To determine its annual property tax rate, a local government can follow the steps below. Following Steps 1 through 3 will yield the variables needed to perform the calculation set forth in Step 4.

Step 1: Determine the unit’s total estimated appropriations (i.e., expenditures) and the amount of money that revenue sources other than the property tax are expected to yield. The difference between the unit’s total estimated expenditures and revenues is the amount necessary to balance the unit’s budget. This total is the “Estimated Required Property Tax Revenue.”

Step 2: Determine the percentage of property taxes collected in the prior fiscal year, expressed as a decimal (e.g., 0.95). This total is the “Last Fiscal Year Collection Percentage.”17

Step 3: Determine the total value of taxable property in the jurisdiction. This total is the “Total Taxable Valuation of Property.”

Step 4: Using the figures from Steps 1 through 3, perform the calculation below. The resulting figure is the rate of property tax per $100.00 assessed valuation.

To illustrate, assume that (1) a unit must obtain $10,000,000.00 in property taxes to balance its budget; (2) its rate of property taxes collected in the prior fiscal year was 95 percent (or 0.95); (3) the unit’s taxable valuation of property is $1.5 billion. Using these figures in the formula above yields a tax rate of $.7017 per $100.00 of assessed valuation.

The governing board of a county or municipality sets its rates of property tax when it adopts its annual budget ordinance—and with very limited exceptions, the governing board may not change a rate of property tax after adopting a budget.18 Property taxes are due on September 1, but taxpayers may delay payment until January 5 without incurring a penalty.19 As a result, local governments typically do not receive the bulk of property taxes owed until the middle of their fiscal year and must rely on fund balances and other revenue sources to finance expenditures during the first part of the fiscal year.

Uniformity of Taxation and Special Taxing Districts

Although the North Carolina Constitution requires that a local government’s rates of property tax be uniform throughout each jurisdiction,20 it also authorizes the General Assembly to permit counties and municipalities to (1) delineate one or more geographic areas within the unit as special taxing districts and (2) levy taxes within those districts to finance or provide services or facilities to a greater extent than those financed or provided in other parts of the jurisdiction.21 The General Assembly has exercised that authority in several cases described below.

Special Taxing Districts

Service Districts

The General Assembly has authorized counties and municipalities to create “service districts.”22 Service districts are geographic areas within which a county or municipality may levy additional property taxes to provide services or capital projects in the district. Counties and municipalities may establish service districts for the respective purposes listed in Table 4.1.

Table 4.1 Primary Purposes for Which Counties and Municipalities May Create Service Districts

Authorized County Service Districtsa

Authorized Municipal Service Districtsb

Beach erosion and flood and hurricane protection works

Fire protection

Recreation

Sewage collection and disposal

Solid waste collection and disposal

Water supply and distribution

Ambulance and rescue services

Watershed improvement, drainage, and water resources development

Cemeteries

Beach erosion and flood and hurricane protection works

Downtown revitalization projects

Urban area revitalization projects

Transit-oriented development projects

Drainage projects

Sewage collection and disposal systems

Off-street parking facilities

Watershed improvement, drainage, and water resources development projects

a. G.S. 153A-301(a)(1)–(11). Counties may create service districts for a few other specified purposes.

b. G.S. 160A-536(a)(1)–(6). Municipalities may create service districts for a few other specified purposes.

Counties most often use service districts to finance the operational and capital expenses of fire and rescue services.23 Municipalities most often use service districts to finance projects and programs in their central business districts.24

Process for Establishing a Service District

Counties and municipalities follow different statutory procedures to establish service districts. Those procedures are detailed in tables 4.2 and 4.3.

Table 4.2 Required Procedures for Establishing a County Service District

Step

Required Action

1a

The governing board must consider

resident or seasonal population and population density of proposed district,

appraised value of property subject to taxation,

present tax rates of the county and any cities or special districts in which the district or any portion thereof is located,

the ability of the proposed district to sustain the additional taxes necessary to provide the services planned for the district, and

any other matters that county commissioners believe might have a bearing on whether the district should be established.

2b

The governing board must find that

there is a demonstrable need for providing one or more authorized services in the district,

it is impossible or impracticable to provide those services on a countywide basis,

it is economically feasible to provide the proposed services in the district without unreasonable or burdensome annual tax levies, and

there is a demonstrable demand for the proposed services by persons residing in the district.

3c

Staff must prepare a report containing

a map of the proposed district, showing its proposed boundaries;

a statement showing that the proposed district meets the standards set out in Step 1; and

a plan for providing one or more of the authorized services.

4d

Staff must make the report available in the office of the clerk to the governing board for at least four weeks prior to the public hearing on the proposed service district.

5e

Staff must prepare notice of public hearing. The notice must include

the date and hour of the hearing,

the place of the hearing,

the subject of the hearing,

a map of the proposed district, and

a statement that the report described in Step 3 is available for public inspection in the office of the clerk to the governing board.

6f

Staff must mail notice to all owners of property in the proposed service district, as reflected in the county tax records on January 1 of the preceding year, at least four weeks prior to the date of the hearing.

7g

Staff must certify in writing to the governing board that the mailing required by Step 6 has been completed.

8h

Staff must publish notice of public hearing at least one week prior to the date of the public hearing on the proposed service district.

9

The governing board must hold a public hearing on the proposed district.

10i

The governing board adopts a resolution establishing the district. The district may take effect at the beginning of a future fiscal year.

f. G.S. 153A-302(c). A county need not mail notice to all property owners if (1) the board proposes to create a service district and (2) the board publishes a notice of proposal to establish the district once per week for four successive weeks before the date of the public hearing on the proposed district. SeeG.S. 153A-302(e) (countywide law enforcement district); 153A-302(f) (countywide districts for counties in which only one incorporated municipality is located within the county but whose land area is located primarily in another county and consists of less than 100 acres in such a county).

Table 4.3 Required Procedures for Establishing a Municipal Service District

Step

Required Action

1

Board-Initiated Processa

The governing board must find that a proposed district is in need of one or more authorized services, facilities, or functions.

OR

Citizen-Initiated Processb

A majority of the owners of real property within a municipality must submit a petition to the governing board establishing that the area is in need of one or more authorized services, facilities, or functions. The petition must contain

the names, addresses, and signatures of the real property owners within the proposed district;

the proposed district boundaries; and

the authorized services, facilities, or functions that would serve as the basis for establishing the proposed district.

2c

Staff must prepare a report containing

a map of the proposed service district, showing its proposed boundaries;

a statement showing that the proposed district meets the standards set out in Step 1; and

a plan for providing one or more of the authorized services.

3d

Staff must make the report available in the office of the clerk to the governing board for at least four weeks prior to public hearing on the proposed service district.

4e

Staff must prepare notice of public hearing. The notice must include

the date and hour of the hearing,

the place of the hearing,

the subject of the hearing,

a map of the proposed district, and

a statement that the report described in Step 3 is available for public inspection in the office of the clerk to the governing board.

5f

Staff must mail notice to all owners of property in the proposed service district, as reflected in the county tax records on January 1 of the preceding year, at least four weeks prior to the date of the hearing.

6g

Staff must certify in writing to the governing board that the mailing required by Step 5 has been completed.

7h

Staff must publish notice of public hearing at least one week prior to the date of the public hearing on the proposed service district.

8i

The governing board must hold a public hearing on the proposed district.

9j

At the public hearing or no later than five days after the date of the public hearing, an owner of a tract or parcel of land located within the proposed service district may submit a written request to the governing board asking that the owner’s tract or parcel be excluded from the proposed district. The request must specify

the tract or parcel for which exclusion is requested;

the particular reason(s) why the tract or parcel is not in need of the services, facilities, or functions of the proposed district to a demonstrably greater extent than the remainder of the tracts and parcels in the municipality; and

any other additional information the owner deems relevant.

10k

If the governing board finds that a tract or parcel for which exclusion is requested is not in need of the services, facilities, or functions of the proposed service district, the board may, but is not required to, exclude the tract or parcel from the proposed district.

11l

At a meeting of the governing board, a majority of voting members present must vote to adopt an ordinance establishing the service district.

The district may take effect at the beginning of a future fiscal year unless the adopting ordinance states that general obligation bonds or special obligation bonds are anticipated to be authorized for the project. In that case, the governing board may make the ordinance effective immediately or as otherwise specified in the ordinance—but the municipality may not levy an ad valorem tax for a partial fiscal year.

12m

At a second meeting of the governing board, a majority of voting members present must vote to adopt an ordinance establishing the service district.

b. G.S. 160A-537(a1). The governing board may, but is not required to, establish a policy to hear all petitions at regular intervals, but no less than once per year. Id.

The governing board may initiate the process of creating a service district upon its own accord—it need not receive a petition from property owners.25 Nor must a county or municipality obtain voter approval via referendum to create a service district. A county service district may not include land within the corporate limits of a city or sanitary district unless the governing body of the city or sanitary district agrees, by resolution, to such inclusion.26

Taxing Authority in a Service District

Under North Carolina law, a service district is not a unit of government. It is instead a geographic designation: a portion of a county’s or municipality’s territory in which the county or municipality, respectively, may levy an extra property tax to provide specific services or capital projects benefitting property within that district.

District Tax Rate

The governing board of a unit that has created a service district may, but is not required to, levy an additional tax upon all taxable properties within the district. A unit that chooses to levy a service-district tax typically sets the district tax rate each year in its annual budget ordinance. The rate of service-district tax, when combined with the unit’s generally applicable rate of property tax, may not exceed $1.50 per $100.00 of assessed valuation of property in the district unless a majority of voters residing within the district approve such a rate.27

Statutory exemptions and exclusions to the property (ad valorem) tax also apply to service-district taxes.28 If real or personal property is exempt from property tax, it also is exempt from service-district tax.

A unit must use all proceeds of service-district taxes to provide services or undertake capital projects in the district,29 but it also may use other unrestricted revenues to provide services or undertake capital projects within the district. A unit may not appropriate proceeds of service-district taxes for other purposes unrelated to the district.30

Providing Services and Projects in a Service District

A municipality may “provide services, facilities, functions, or promotional and developmental activities in a service district with its own forces, through a contract with another governmental agency, or by any combination thereof.”31 If a county or municipality levies a service-district tax, it must “provide, maintain, or let contracts for” the services involved within a reasonable time not exceeding one year.32 In addition, a contract between a municipality and a third-party service provider must

specify the purposes for which municipal funds will be used;

require an appropriate accounting of moneys paid out under the contract at the end of a fiscal year (or another appropriate period of time); and

if the contract is between a municipality and a private agency, require the private entity to provide certain information about subcontractors, including “the name, location, purpose, and amount paid to any person or persons with whom the private agency contracted to perform or complete any purpose for which [municipal] moneys were used for that service district.”33

A municipality that contracts with a private third-party service provider in certain historic district overlay service districts and in service districts created for downtown revitalization or urban area revitalization also must (1) require the private provider to report annually to the municipality; (2) specify, by contract, the scope of services to be provided; and (3) limit any contract to a term of five years or less.34 Such a municipality also must (1) solicit public input from district residents prior to entering into a contract; (2) use a bid process to select the private provider; and (3) hold a public hearing on the proposed contract, with notice of the hearing published in a newspaper of general circulation for at least two successive weeks prior to the hearing.35

Borrowing Money to Fund Capital Projects in a Service District

In general, a county or municipality may borrow money to fund capital projects located in a service district to the same extent, and in the same manner, as it funds similar projects outside of a service district. For more detailed information on this topic, see Chapter 7, “Financing Capital Projects.”

Other Special Taxing Districts

Counties also may establish special taxing districts for rural fire-protection services,36 public schools,37 and water and sewer services.38 These districts provide counties with additional mechanisms to fund capital and operating expenses for the statutorily specified purposes. For a county to levy a tax for rural fire protection or public schools, a majority of qualified county voters voting in a referendum must approve the tax.39

Local Sales and Use Taxes

North Carolina sales and use taxes are comprised of two components: (1) a tax on the retail sale of certain “items” (including tangible personal property, certain digital property, and some services)40 and (2) a complementary “use” tax on (a) tangible personal property purchased, leased, or rented for storage or use in North Carolina; (b) certain digital property purchased for storage or use in the state; or (c) services sourced to North Carolina.41 Where a retailer fails to collect sales tax upon a taxable sale, the individual or entity that uses the item sold must pay use tax at an equivalent rate of tax.42

The State of North Carolina levies statewide sales and use taxes upon certain items—generally at a rate of 4.75 percent—but certain types of local governments also may levy “local” sales and use taxes that apply apart from this statewide rate. This section describes (1) which local governments may impose “local” sales and use taxes, (2) how local sales and use taxes are collected, and (3) how the proceeds of local sales and use taxes are allocated among each county and distributed for use.

Authority to Impose Local Sales and Use Taxes

Only counties—not municipalities within those counties—may levy local sales and use taxes. As of July 1, 2023, Chapter 105 of the General Statutes provides that authority to counties in four separate articles: Article 39 (authorizing the imposition of a 1-cent tax); Article 40 (authorizing the imposition of a 0.5-cent tax); Article 42 (authorizing the imposition of a 0.5-cent tax); and Article 46 (authorizing the imposition of a 0.25-cent tax). As of December 31, 2022, all counties levy Article 39, 40, and 42 taxes, but only 47 counties levy Article 46 taxes.43 Counties may levy Article 46 taxes only with voter approval.44

Each Article sets out the sales and uses to which its sales and use taxes apply. The tax bases for local sales and use taxes and statewide sales and use taxes are not identical.45 For example, sales of non-prepared food (i.e., groceries) are not subject to statewide sales and use tax but are subject to Article 39, 40, and 42 taxes.46

Collection of Local Sales and Use Taxes

Retailers must collect local sales taxes in connection with each taxable sale and remit the proceeds to the North Carolina Department of Revenue (NCDOR).47 If a retailer fails to collect sales tax, the purchaser or user of an item must remit use tax—at a rate equivalent to the rate of applicable sales tax—to NCDOR.48 Counties and municipalities have no legal obligation or authority to collect local sales or use taxes from public or private organizations with such liabilities.

Allocation of Local Sales and Use Taxes

Once NCDOR collects local sales and use taxes, it allocates the revenues of each local sales and use tax according to restrictions contained in each local sales and use tax Article.

NCDOR allocates the revenues of Article 39 and 42 taxes to counties on a point-of-origin basis, meaning generally that NCDOR sources proceeds of each tax to the county in which the purchased goods are delivered.49 NCDOR allocates the revenues of Article 40 taxes among counties on a per capita basis, meaning that the allocation is based solely upon the relative population of each county—not upon the amount of taxable transactions occurring in each jurisdiction.50 NCDOR allocates the revenues of Article 46 taxes to the counties in which the purchased goods are delivered.51

By statute, NCDOR makes further adjustments to these initial allocations. For example, NCDOR adjusts each county’s initial per capita allocation of Article 40 taxes by multiplying that allocation by an “adjustment factor” for each county specified in the General Statutes.52 This adjustment causes some counties to receive more and some counties to receive less in Article 40 taxes than they would receive under a pure per capita allocation.

The statutes also direct NCDOR to further adjust the allocations of Article 39, 40, and 42 taxes. In particular, it must place a portion of each of these taxes into a separate “statewide pool” created under Article 44 of G.S. Chapter 105.53 Beginning in Fiscal Year 2016–2017, the General Statutes directed NCDOR to place a total of $84,800,000.00, deducted and divided proportionately from Article 39, 40, and 42 taxes otherwise allocated to each county, into this Article 44 “statewide pool.”54 In each fiscal year following Fiscal Year 2016–2017, NCDOR has adjusted and will continue to adjust this total amount based upon the annual percentage change in Article 39, 40, and 42 collections. NCDOR allocates the “statewide pool” to each county based upon an “allocation percentage,” which results in seventy-nine generally more rural counties receiving an allocation and twenty-one generally more urban counties not receiving an allocation from the statewide pool.55

Distribution of Local Sales and Use Tax Proceeds

On a monthly basis, NCDOR distributes the allocated proceeds of local sales and use taxes under Articles 39, 40, 42, and 46, as well as the Article 44 statewide pool.56

Distributions of Article 39, 40, 42 Taxes and Article 44 Statewide Pool Moneys

Although NCDOR allocates all the proceeds of Article 39, 40, and 42 taxes and Article 44 statewide pool moneys to counties, it ultimately does not distribute all of these proceeds to counties. Instead, the General Statutes direct NCDOR to distribute a portion of the proceeds of these taxes to municipalities.

North Carolina law entitles the governing board of each county to annually choose one of two methods that NCDOR must follow to distribute the allocated proceeds of Article 39, 40, and 42 taxes and Article 44 statewide pool moneys to counties and municipalities located within their county: (1) the per capita method, under which NCDOR divides and distributes the proceeds of taxes allocated to each county between the county and each municipality located in the county based upon their relative populations, or (2) the ad valorem method, under which NCDOR divides and distributes the proceeds of taxes allocated to each county based upon the relative property tax levies of the county and each municipality located in the county.57

Boards of county commissioners must make this choice each April. After August 2021, any change in a method is effective as of the fiscal year following the succeeding fiscal year after the change occurs.58 For example, a county’s election to change distribution methods in April 2023 would become effective as of July 1, 2024.

Distributions of Article 46 Taxes

NCDOR distributes the allocated proceeds of Article 46 taxes only to counties.59 Counties that levy Article 46 taxes are neither required nor authorized to share the proceeds of those taxes with their municipalities or other taxing units in the county.

Use of Local Sales and Use Tax Proceeds

Municipalities that receive distributions of Article 39, 40, and 42 tax proceeds or Article 44 statewide pool proceeds may use these moneys for any public purposes for which they have legal authority to expend funds.

Counties must reserve a portion of local sales tax proceeds that they receive for specific purposes. In particular, a county must reserve 60 percent of Article 42 tax proceeds and 30 percent of Article 40 tax proceeds for public school capital outlay or debt service incurred for public school construction projects.60 A county also must use any proceeds of a distribution of Article 44 statewide pool proceeds for “economic development, public education, and community college” purposes.61 Counties may use all other proceeds of Article 39, 40, and 42 taxes for any public purpose for which counties are authorized to engage.

“Hold Harmless” Payments and State Contributions

Medicaid Hold Harmless

In 2007 and 2008, the General Assembly adopted legislation that (1) limited and amended county and municipal authority to impose local sales and use taxes and (2) directed that the state assume responsibility for Medicaid expenses previously covered by county governments.62 Under this legislation, counties must hold municipalities incorporated before October 1, 2008, harmless for the revenue that such a municipality would have received from a formerly authorized 0.50 percent local sales and use tax under Article 44 of G.S. Chapter 105 that was distributed on a point-of-origin basis.63 In other words, each of these municipalities must continue to receive the equivalent amount of revenue were that tax still in effect.

The General Statutes calculate that sum by adding (1) the proceeds of Article 40 sales and use tax allocated to a municipality (the “base hold harmless amount”) to (2) 50 percent of the base hold-harmless amount less 25 percent of Article 39 sales and use tax proceeds allocated to a municipality.64 The “base hold-harmless amount” accounts for the loss of Article 44 tax revenue, while the latter figure accounts for a change in distribution method in half of Article 42 sales and use tax proceeds from per capita to point-of-origin. NCDOR adds this total hold-harmless payment to the distributions of other local sales and use taxes that municipalities receive and derives the revenue to make this distribution from each county’s allocation of Article 39 sales and use tax proceeds.65

Since Fiscal Year 2017–2018, the General Assembly has guaranteed to counties that if (1) the sum of the annual amount a county would have received from formerly-imposed Article 44 sales and use taxes (the “repealed sales tax amount”)66plus the amount the county is required to pay to its municipalities to hold them harmless for the repeal of Article 44 sales and use taxes exceeds (2) the amount that the state assumed for the county’s proportionate share of Medicaid costs, then the state shall pay that difference to a county.67 NCDOR estimates all of these figures for a fiscal year and sends to eligible counties 90 percent of its estimated payment for that fiscal year with other sales tax distributions in March.68 NCDOR then determines the actual estimated payment for the fiscal year by August 15 of the next fiscal year and remits the remaining balance to eligible counties.69

Transportation Sales and Use Taxes

Under Article 43 of G.S. Chapter 105, counties and certain transportation authorities also may levy an additional type of local sales tax—a transportation sales and use tax—to fund public transportation systems. Mecklenburg County; a regional transportation authority encompassing Wake, Durham, and/or Orange County; and a regional transportation authority encompassing Forsyth and/or Guilford Counties each may adopt a 0.5-cent sales and use tax.70 All other counties may levy a 0.25-cent transportation sales and use tax.

Governing boards of these units of local government may levy a transportation sales and use tax only after voters approve such a levy by referendum.71 The proceeds of transportation sales and use taxes are allocated either to (1) one or more special districts that a regional transportation authority creates72 or (2) on a per capita basis among the county and other units of local government in the county that operate public transportation systems.73 In each case, counties, municipalities, and regional transportation authorities may only use the proceeds of transportation sales and use taxes for financing, constructing, operating, and maintaining public transportation systems.74

Other Local Taxes

The General Statutes authorize counties and municipalities to levy several other types of taxes, including a rental car gross receipts tax, an animal tax, a heavy equipment rental tax, and motor vehicle license taxes. The General Assembly also has authorized, via separate local acts, certain counties and municipalities to levy a variety of taxes, including occupancy taxes, prepared food and beverage taxes, deed transfer taxes, and motor vehicle taxes. This section details taxes authorized by general law and local act. Although these local taxes make up a relatively insignificant proportion of the total revenues that North Carolina’s local governments receive, they produce, at a minimum, hundreds of thousands of dollars for many counties and municipalities—and even more for some of the state’s largest local governments.

Taxes Authorized by General Law

Except for county motor vehicle license taxes and a portion of municipal motor vehicle license taxes, counties and municipalities may use the revenues from the taxes described in this section for any public purpose for which they may spend funds under general law.

Rental Car Gross Receipts Tax

Counties and municipalities may, but are not required to, levy a gross receipts tax on the “short-term lease or rental” of vehicles at retail.75 The maximum rate of such tax, where levied, is 1.5 percent of the gross receipts derived from the short-term lease or rental of vehicles.76

Animal Tax

Counties and municipalities may levy taxes on the privilege of keeping an animal.77 A local government may decide which domestic animals it may tax and the rates of tax it will charge. Rates often vary based upon the type of animal and whether the animal has been spayed or neutered. Units often charge higher rates to animals that have not been spayed or neutered. A unit of local government may use the proceeds of these taxes for any authorized public purpose.78

Short-Term Heavy Equipment Rentals Tax

Counties and municipalities may levy a tax on the gross receipts of individuals or entities whose principal business is the “short-term lease or rental” of “heavy equipment” at retail.79 “Heavy equipment” includes “[e]arthmoving, construction, or industrial equipment that is mobile” and that is either (1) “a self-propelled vehicle that is not designed to be driven on a highway” or (2) “industrial lift equipment, including material handling equipment, industrial electrical generation equipment, or a similar piece of industrial equipment.”80

A county may, by resolution, impose a tax at a rate of 1.2 percent of gross receipts derived from the short-term lease or rental of heavy equipment if the place of business from which the equipment is delivered is located in the county.81 A municipality may, by ordinance, impose a tax at a rate of 0.8 percent of gross receipts derived from the short-term lease or rental of heavy equipment if the place of business from which the equipment is delivered is located in the municipality.82 Where imposed, these taxes are payable quarterly to the respective unit and due by the last day of the month following the end of each calendar quarter.83

Motor Vehicle License Taxes

Municipalities may levy an annual motor vehicle license tax of up to $30.00 upon individuals or entities for the privilege of keeping a vehicle within the municipality.84 A municipality is bound by the following restrictions when using the proceeds of these taxes:

the municipality may use up to $5.00 of the proceeds for any lawful purpose;

if it operates a “public transportation system” (as defined in G.S. 105-550),85 it may use up to $5.00 of the proceeds for financing, constructing, operating, and maintaining such local public transportation system; and

the municipality may use the remainder of the tax for “maintaining, repairing, reconstructing, widening, or improving public streets in the [municipality] that do not form a part of the State highway system.”86

The General Assembly has authorized some municipalities, via local act, to levy motor vehicle license taxes to be used in amounts and for purposes other than those identified above.87

A county may levy an annual vehicle registration tax of up to $7.00 for each vehicle located within the county if it—or a municipality within the county—operates a “public transportation system.”88 A levying county must distribute the proceeds of these taxes to municipalities operating a “public transportation system,” if any, on a per capita basis.89 The county and any recipient municipalities must use the proceeds of such taxes to finance, construct, operate, or maintain a public transportation system.90

Municipalities may levy an annual tax of up to $15.00 on each vehicle operated as a taxicab within the municipality—and may use the proceeds of such taxes for any public purpose.91 Municipalities and counties have no legal authority, however, to extend this tax to vehicles used by drivers for a transportation-network company (TNC) (e.g., Uber or Lyft).92

Privilege License Taxes

For fiscal years beginning on or after July 1, 2015, neither a municipality nor a county may assess or collect a privilege license tax.93 Prior to that date, the General Assembly authorized municipalities and counties—albeit in differing forms—to levy taxes upon the privilege of carrying on a business or engaging in certain types of occupations, trades, employment, or activities.94

Malt Beverage and Wine License Taxes

When it prohibited the county and municipal imposition of privilege license taxes, the General Assembly did not revoke the authority of counties and municipalities to charge similar license taxes applicable to the retail sale or wholesale of malt beverages (i.e., beer) and wine.

Entities and individuals that sell beer and wine at retail must obtain certain permits from the North Carolina Alcoholic Beverage Control (ABC) Commission.95 These permit holders must obtain a malt beverage or wine license from the county and municipality, if any, in which the selling establishment is located.96 The corresponding tax for each type of license ranges from $5.00 to $25.00.97

A municipality may also require a business “located inside the city” that acts as a wholesaler of beer or wine to obtain a license to engage in such activity and pay a corresponding tax.98 Such a tax may not exceed $37.50. The General Assembly has not granted comparable authority to counties.

A county or municipality may use the proceeds of malt beverage and wine license taxes or wholesaler license taxes for any lawful purpose.

Business Registration Fees

Municipalities and counties may “by ordinance . . . regulate and license occupations, businesses, trades, professions, and forms of amusement or entertainment and prohibit those that may be inimical to the public health, welfare, safety, order, or convenience.”99 With two exceptions, each entity likely has legal authority to require businesses with a physical location within their jurisdiction to (1) register with the respective municipality or county and (2) charge a reasonable fee to businesses in connection with such registration.100 The charging unit of local government must use the proceeds of these fees to operate the business-registration program.

Taxes Permitted by Local Act

Occupancy Taxes

As of November 2022, the General Assembly has granted authority to units of local government in more than seventy counties, via local act, to levy occupancy taxes.101 With some exceptions, these taxes generally apply to the short-term use or rental of an “accommodation”—“a hotel room, a motel room, a residence, a cottage, or a similar lodging facility for occupancy by an individual.”102 Counties levy most of these taxes, and many of the local acts authorizing such taxes require a county to distribute a portion of these taxes to municipalities.103 Many of the local acts also restrict the use of proceeds to particular purposes—most commonly, to purposes related to travel or tourism—but some permit the use of the proceeds for any public purpose.104

Prepared Food and Beverage Taxes

The General Assembly has authorized several counties and municipalities to levy taxes on the retail sale of prepared food and beverages.105 The local acts authorizing the imposition of such a tax typically restrict the amount of the tax and the purposes for which the collecting unit of local government may spend the tax proceeds.106 Where a unit of local government has levied taxes upon the sale of prepared food and beverages, state and local option sales taxes may also apply.

Real Estate Transfer Taxes

The General Assembly has authorized seven coastal counties to assess an excise tax of 1 percent upon certain conveyances of real property in each county.107 The local acts authorizing the imposition of such taxes typically restrict the purposes for which the collecting county may spend the tax proceeds.108

Local Fees, Charges, and Assessments

Local governments do not rely solely upon the proceeds of taxes to fund the services that they provide. Units of local government have access to a variety of other revenue sources other than taxes, and most fall into the following six categories: (1) general user fees and charges, (2) regulatory fees, (3) public enterprise fees and charges, (4) franchise fees, (5) statutory fees, and (6) special assessments.

General User Fees and Charges

Many units of local government now rely upon mechanisms for targeted revenue generations like user fees and charges, which are paid only by the citizens or property owners that benefit most directly from a service that unit provides. These types of fees and charges are typically an appropriate funding source for services that have specific, identifiable beneficiaries rather than the public at large.109

A unit of local government typically accounts for revenue generated from general user fees and charges in its general fund, and, unless state law restricts the expenditure of these fees and charges, a unit may use these fees for any lawful purpose. The General Assembly may grant express legal authority in the General Statutes or in a local act to a unit of local government to assess a user charge or fee; a unit of local government also may assess a user charge or fee where legal authority to assess a user charge or fee can reasonably be implied from the legislature’s authorization for a unit of local government to conduct an activity or provide a service.

Units of local government commonly fund a variety of services at least in part through general user fees and charges, including recreation and cultural activities, art galleries and museums, auditoriums, coliseums, convention centers, emergency medical services, on- and off-street parking, cemeteries, certain public health services, and certain mental health services.

Regulatory Fees

A regulatory fee is a charge assessed to cover the cost of performing a regulatory program or service that a local government may or must provide. In some cases, the General Statutes expressly authorize a county or municipality to charge a fee for the performance of a regulatory activity. For example, a municipality may “regulate all vehicles operated for hire” in its jurisdiction and require all “drivers and operators of taxicabs” to obtain a license or permit from the city at a cost not to exceed $15.00.110 In other cases, though, the General Statutes authorize a county or municipality to perform a regulatory function but do not contain explicit authority to impose a fee or charge upon a person or entity that the local government is regulating. For example, municipalities have express statutory authority to adopt an ordinance that “regulate[s], restrict[s] or prohibit[s] . . . the business activities of itinerant merchants, salesmen, promoters, drummers, peddlers, flea market vendors and hawkers” and requires that these individuals receive a municipal permit to engage in these business activities.111 That statutory authority does not, however, expressly authorize municipalities to charge a fee for the issuance of such a permit. In that case, do municipalities have implied legal authority to impose such a fee?112

In a 1994 ruling—Homebuilders Association of Charlotte, Inc. v. City of Charlotte—the North Carolina Supreme Court held that the legal authority of a local government to charge a fee may be implied from express statutory authority to engage in a regulatory activity.113 But the court also held that such regulatory fees charged must be “reasonable”—in other words, not exceeding the direct and indirect costs of performing the regulatory activity—and used for the sole purpose of defraying the cost of regulation.114 The state supreme court has issued a number of subsequent decisions that apply and interpret the 1994 Homebuilders ruling,115 and a local government should work closely with its legal counsel prior to relying upon implied authority to impose a fee or charge.

At present, county boards of commissioners have express authority to set fees and charges for services or duties that county officers or employees may or must perform.116 Although no analogous statute applies to municipalities, a municipality may have implied authority to impose a reasonable fee or charge for performance of a regulatory function and use the proceeds of that fee to defray the cost of the function.

Local governments continue to commonly assess regulatory fees to cover the costs of performing certain regulatory activities like issuing building permits, evaluating environmental impacts, reviewing development plans, and enforcing other local ordinances. Prior to the General Assembly’s 2020 comprehensive revision and restatement of North Carolina’s land use and planning laws in G.S. Chapter 160D, counties and municipalities had express statutory authority to “fix reasonable fees for issuance of permits, inspections, and other services of an inspections department” and to use any such fees collected “for support of the administration and activities of the inspection department and for no other purpose.”117 Now, this statutory authority permits counties and municipalities to “fix reasonable fees for support, administration, and implementation of programs authorized by . . . Chapter [160D], and [to use] such fees . . . for no other purposes.”118 Chapter 160D authorizes counties and municipalities to engage in a range of regulatory programs, including, among other things, issuing building permits, performing inspections of structures, and approving plats for the subdivision of land.119

Typically, a unit of local government adopts a schedule of fees on an annual basis. Although the General Statutes do not prescribe formal procedural requirements to adopt or amend fees or a fee schedule, the General Statutes impose certain procedural requirements upon the imposition or increase of fees or charges applicable solely to the development of subdivisions.120

Public Enterprise Fees and Charges

Counties and municipalities have legal authority to operate a range of public enterprises.121 Public enterprises are activities of a commercial nature that the private sector could provide but that the public sector has chosen to provide. The most common public enterprises that North Carolina’s counties and municipalities operate are water supply and distribution systems, sewage collection and treatment, and solid waste collection and disposal utilities. But counties and municipalities also may legally operate other types of public enterprises, including airports, public transportation, off-street parking facilities, and stormwater systems, and municipalities have additional authority to operate public enterprises for electric power generation and distribution, gas production and distribution, and cable television.122

A unit of local government that provides public enterprises may assess a variety of fees and charges to cover the capital and operating expenses necessary to operate those public enterprises. Many of these public enterprises are self-supporting, meaning that the revenue the enterprise generates through fees and charges is sufficient to cover the cost of providing services. Chapter 13, “Financing Public Enterprises,” outlines the legal authority of counties and municipalities to impose fees and charges for public enterprise activities.

Franchise Fees

A franchise is a legal privilege to engage in a type of business in the boundaries of a particular jurisdiction. With authorization from the General Assembly, North Carolina’s counties and municipalities may grant franchises to private entities to engage in a variety of activities. However, authority to grant a franchise does not necessarily include authority to charge a franchise fees. Counties have authority to grant franchises and charge licensing fees for solid waste collection and disposal.123 Municipalities can grant franchises for a much wider range of purposes, including airports, ambulance companies, off-street parking, and solid waste collection and disposal.124 Municipalities also may grant franchises and charge franchise fees for taxicabs.125

Statutory Fees

The General Statutes establish a variety of fees that units of local government—and, in particular, specific offices within units of local government—must or may charge. This section details a number of statutory fees collected or received by units of local government.

Fees of Public Officers

Sheriff

A county sheriff may collect a variety of fees. Among others, a county sheriff is entitled to collect fees from a convicted defendant for arresting that defendant or serving that individual with criminal process,126 fees for providing pretrial release services to such a defendant,127 and fees for lawfully confining an individual in jail prior to trial.128 A county sheriff also may collect fees for the service of civil process129 and the sale of real or personal property to satisfy a judgment.130

Register of Deeds

Registers of deeds collect fees in connection with the wide variety of services that they perform.131 Although fees for recording deeds and other legal instruments affecting titles to real property make up the bulk of the fees that registers of deeds collect, other major sources of revenue include fees for issuing marriage licenses. In many counties, the register of deeds collects fee revenue that exceeds the costs of operating its office.

On a monthly basis, each county must deposit with the North Carolina Department of State Treasurer an amount equal to 1.5 percent of the fees collected by registers of deeds under G.S. 161-10.132 Counties must remit portions of other fees collected under G.S. 161-10 to a variety of other state-level entities for specific purposes.133

Court Facilities and Related Fees

The state assesses fees against criminal defendants and civil litigants to help offset the cost of operating state courts. These fees include a variety of “facilities” fees: (1) a fee assessed to a convicted criminal defendant to be remitted to the unit of local government (most commonly, a county) that provides the judicial facility in which judgment is rendered;134 (2) a fee assessed in civil actions to be remitted to the unit of local government (most commonly, a county) that provides the judicial facility in which judgment is rendered;135 (3) a fee assessed for special proceedings in superior court, to be remitted to the county;136 and (4) a fee assessed for the use of a courtroom and related judicial facilities in, among other things, the administration of the estates of decedents, minors, incompetents, and missing persons, to be remitted to the county.137 The proceeds of all these fees must be used by the recipient for “providing, maintaining, and constructing adequate and related judicial facilities.”138

Special Assessments

A special assessment is a charge levied against real property to pay for public improvements that benefit that property. It is neither a user charge nor a tax but shares characteristics of each. Like a user charge, a special assessment is levied in some proportion to the benefit that the assessed property receives. But like a property tax, it is levied against property rather than individuals and creates a lien on each parcel of real property assessed.139

Counties and municipalities in North Carolina may use special assessments to fund certain capital improvement projects.140Chapter 7, “Financing Capital Projects,” discusses special assessments in detail.

State Revenues Shared with Local Governments

The State of North Carolina generates certain revenues that it shares with units of local government. State officials, rather than local officials, bear the political burden of imposing these revenues, but local governing boards largely lack control over their imposition or distribution. The General Assembly may at any time reduce or eliminate the sources of revenue that it shares with units of local government.

The state currently shares a variety of tax and fee revenues with counties: video programming services taxes, malt beverage and wine taxes, solid waste tipping taxes, real estate transfer taxes, disposal taxes, and a 911 charge upon voice communication services. With the exception of real estate transfer taxes and disposal taxes, the state also shares a portion of each of those revenues with municipalities. Municipalities also receive a portion of state-levied electric franchise taxes, telecommunications taxes, piped natural gas taxes, and motor fuels taxes. This section explains each of these state revenue sources in more detail.

Video Programming Services Taxes

The General Assembly has levied a statewide sales tax—at the “combined general rate”141 of 7.0 percent—upon sales of video programming services (including direct-to-home satellite services).142 The North Carolina Department of Revenue (NCDOR) collects these taxes and, on a quarterly basis and within seventy-five calendar days of the end of each calendar quarter, distributes a portion of the proceeds of these taxes—along with a portion of the proceeds of state sales taxes levied upon telecommunication services—to counties and municipalities.143 In particular, NCDOR must distribute: (1) 7.7 percent of the net proceeds of taxes collected during the quarter upon telecommunications services, (2) 23.6 percent of the net proceeds of taxes collected during the quarter on video programming services other than direct-to-home satellite services, and (3) 37.1 percent of the net proceeds of taxes collected during the quarter on direct-to-home satellite services.144 The following sections explain how NCDOR distributes these proceeds.

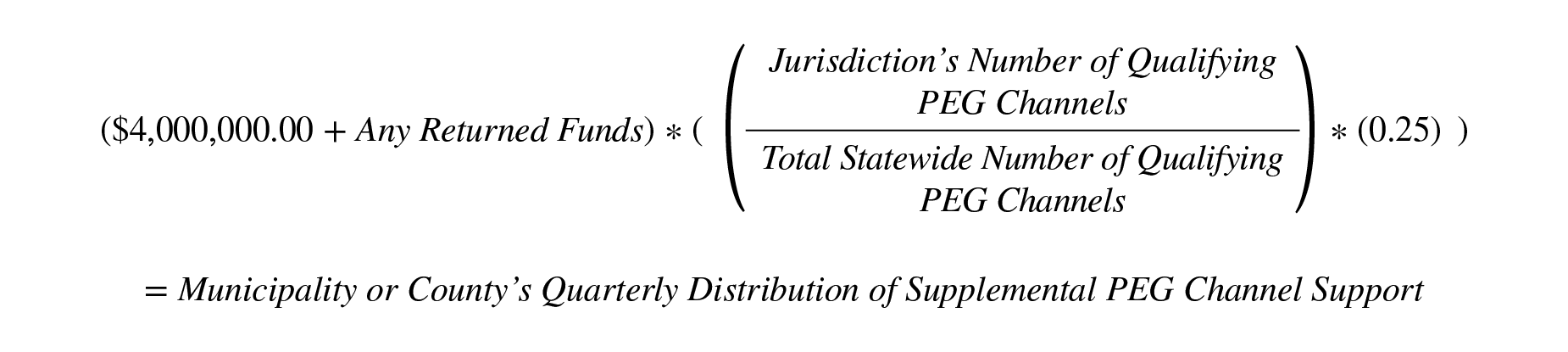

Distribution of Supplemental “PEG Channel” Support

First, NCDOR distributes a portion of the proceeds of these taxes to municipalities and counties that operate “qualifying PEG channels.” A “qualifying PEG” channel is a public, educational, or governmental access channel provided to a county or city that operates for at least ninety days during a fiscal year and that (1) delivers at least eight hours of scheduled programming a day, (2) delivers at least six hours and forty-five minutes of scheduled non-character-generated programming a day, and (3) does not repeat more than 15 percent of the programming content on any other PEG channel provided to the same county or municipality.145

By July 15 of each fiscal year, counties and municipalities that operate qualifying PEG channels must certify to NCDOR all of the qualifying PEG channels provided for its use during the preceding fiscal year.146 Based upon these certifications, NCDOR determines a share to be distributed to each certifying county and municipality on a quarterly basis. The General Statutes direct NCDOR to divide $4,000,000.00 in the proceeds of the taxes identified above, plus any funds returned to NCDOR due to a county or municipality’s improper certification of a PEG channel, among each certifying county and municipality in proportion to the total number of qualifying PEG channels statewide.147 The formula is set forth below.

A county or municipality that receives a distribution of supplemental PEG channel support payments must use such moneys for the operation and support of each qualifying PEG channel and must distribute the funds to a PEG channel operator within thirty days of receipt.148

Remaining Proportionate Share

NCDOR then distributes the net proceeds of the taxes remaining after the distribution of supplemental PEG channel support funds. It determines the amount of this distribution according to each municipality and county’s “proportionate share.”149 A unit’s proportionate share is the ratio of its “base amount” to the sum of the “base amount” for all municipalities and counties. A “base amount” is (1) for any unit that imposed a cable franchise tax before July 1, 2006—the amount of cable franchise tax and subscriber fee revenue that the county imposed from July 1, 2006, through December 31, 2006, or (2) for any unit that did not impose a cable franchise tax before July 1, 2006—the unit’s most recent annual population estimate times $2.00.150 For fiscal years following the 2007 fiscal year, NCDOR further adjusts the “proportionate share” of each county and municipality to account for its growth or decline in population in the preceding fiscal year.151

Restrictions on Use of Proceeds

A county or municipality that imposed subscriber fees between July 1, 2006, and December 31, 2006, must use a portion of these funds to provide for the operation and support of PEG channels.152 In addition, a county or municipality that used a portion of its franchise tax revenue in fiscal year 2005–2006 for the operation and support of PEG channels or for a publicly owned and operated television station must use funds distributed to it to continue the same level of support for such channels and public stations. A county or municipality, after reserving funds for these purposes, may use remaining funds for any public purpose.

Malt Beverage and Wine Taxes

The State of North Carolina levies several taxes on the sale of alcoholic beverages, including excise taxes on malt beverages (i.e., beer) and wine.153 The state distributes a portion of these excise taxes to municipalities and counties: 20.47 percent of the net amount of taxes collected on the sale of malt beverages; 49.44 percent of the net amount of taxes collected on the sale of unfortified wine; and 18 percent of the net amount of taxes collected on the sale of fortified wine.154

A municipality or county may receive a share of this distribution only if beer or wine legally may be sold within its boundaries.155 North Carolina permits the sale of beer and wine throughout the state but permits counties to hold an election in which voters may prohibit “on-premises” or “off-premises” sales of malt beverages and unfortified wine.156 A municipality located within a county in which such sales have been prohibited by election may hold a subsequent election to permit the sale of malt beverages and unfortified wine.157 A municipality or county that only permits the sale of one type of beverage may only share in the proceeds of excise taxes levied upon the type of beverage that may be sold.158

The North Carolina Department of Revenue (NCDOR) distributes the proceeds of these excise taxes to eligible counties and municipalities based upon the ratio of the recipient unit’s population to the population of all eligible counties and municipalities.159 NCDOR must distribute the revenue within sixty days of March 31 and typically makes the distribution on an annual basis.160 Counties and municipalities that receive a distribution may spend the proceeds for any authorized public purpose.

Solid Waste Disposal Taxes

The State of North Carolina imposes an excise tax throughout the state—at a rate of $2.00 per ton—upon the (1) disposal of municipal solid waste and construction and demolition debris in any landfill for which the North Carolina Department of Environmental Quality (NCDEQ) has granted a permit and (2) transfer of municipal solid waste and construction and demolition debris to a transfer station to which NCDEQ has granted a permit.161 Either the owner or operator of each landfill and transfer station must collect the tax and remit the tax to NCDOR.162

After retaining a portion of the proceeds of these taxes as compensation for its cost of collection, NCDOR distributes 18.75 percent of the proceeds of these taxes to eligible counties and 18.75 percent of the proceeds of these taxes to eligible municipalities.163 To be eligible to receive a distribution, a county or municipality must provide, or contract and pay for, solid waste management programs or services.164 NCDOR then makes distributions to eligible counties and municipalities based upon their relative populations.165 Recipient counties and municipalities may only use the proceeds of this distribution to fund solid waste management programs and services.166

Real Estate Transfer Tax

The State of North Carolina imposes an excise tax upon legal instruments recorded with registers of deeds that convey an interest in real property.167 The tax is levied at a rate of $1.00 per $500.00 of the consideration paid for the interest.168 For example, if an individual sells an acre of land for $100,000.00, the excise tax upon the deed that conveys the property would total $200.00.

The register of deeds for the county in which the real property is located collects any tax due and remits the proceeds to such county’s finance officer.169 After retaining up to 2 percent of the proceeds as compensation for the cost of collecting the excise tax, the finance officer must credit one-half of the proceeds to the county’s general fund and remit the other one-half to NCDOR.170 The county may use its portion of the excise tax for any authorized public purpose.

Scrap Tire Disposal Tax

The state imposes and collects a tax upon the sale of new automobile tires sold by a retailer, or sold by a retailer wholesale merchant to a wholesale merchant or retailer, for placement on a vehicle offered for sale, lease, or rental by the retailer or wholesale merchant.171 After retaining a portion of the proceeds of these taxes as compensation for its cost of collection, NCDOR distributes 70 percent of the proceeds of these taxes to counties on a per capita basis.172 A county may use the proceeds of these taxes only for the disposal of scrap tires or the abatement of a tire collection site that constitutes a nuisance.173

White Goods Disposal Tax

The state imposes and collects a tax upon the retail sale of “white goods.”174 After retaining a portion of the proceeds of these taxes as compensation for its cost of collection, NCDOR distributes 70 percent of the proceeds of these taxes to counties on a per capita basis.175 A county may use the proceeds of these taxes only for the management of discarded white goods.176

911 Service Charge

Since 2008, the North Carolina 911 Board—now contained within the State Department of Information Technology—has overseen a consolidated, statewide plan to administer 911 systems and communications between public safety answering points (PSAPs) that call and dispatch public safety agencies for response to a 911 call.177

The state levies a monthly 911 service charge on each (1) active voice communications service connection that provides access to the 911 system and (2) retail purchase of prepaid wireless telecommunications services.178 The 911 Board maintains revenues derived from these service charges in a state-level 911 Fund, from which it makes certain distributions to, among other entities, “primary PSAPs”—entities that serve as the first point of reception for a 911 call.179

The 911 Board must make monthly distributions to eligible primary PSAPs from the 911 Fund based upon a funding formula.180 To receive a distribution from the 911 Fund, a local government must (1) serve as a primary PSAP, (2) provide “enhanced 911 service,”181 and (3) have received distributions from the 911 Board in the 2008–2009 fiscal year.182 It also must comply with a host of other requirements.183

A primary PSAP may use the 911 charge proceeds only for certain expenditures specified by statute. In particular, it may use distributions provided after July 1, 2021, to pay for

the lease, purchase, or maintenance of (a) emergency telephone equipment, including necessary computer hardware and software; (b) telecommunicator failure; (c) dispatch equipment located exclusively within a building where a PSAP or back-up PSAP is located (but excluding the costs of base-station transmitters, towers, microwave links, and antennae used to dispatch emergency-call information from the PSAP or back-up PSAP); or (d) emergency medical, fire, and law enforcement pre-arrival instruction software;

costs incurred by a city or county that operates a PSAP to comply with the terms of certain intergovernmental support agreements with a military installation;

expenditures for in-state training of 911 personnel regarding the maintenance and operation of the 911 system; and

charges associated with a service supplier’s 911 service and other service supplier recurring charges (but excluding service supplier 911 service and other recurring charges supplanted by the state ESInet costs paid by the 911 Board).184

The 911 Board must notify each primary PSAP of its estimated distribution by December 31 of each year and determine actual annual distributions by June 1.185 The PSAP must deposit any funds received into a special revenue fund designated as the Emergency Telephone System Fund.186

A PSAP may carry forward distributions for eligible expenditures for capital outlay, capital improvements, or equipment replacement.187 If the amount carried forward exceeds 20 percent of the average yearly amount distributed to the PSAP in the prior two years, the 911 Board may reduce the PSAP’s distribution.188

Electricity Taxes

The General Assembly has levied a statewide sales tax—at the “combined general rate”189 of 7.0 percent—upon sales of electricity.190 The North Carolina Department of Revenue (NCDOR) collects these taxes and, on a quarterly basis and within seventy-five calendar days of the end of each calendar quarter, distributes a portion of the proceeds of these taxes to municipalities.191 In particular, NCDOR must distribute 44 percent of the net proceeds of taxes collected on electricity less NCDOR’s costs of administering such distribution.192

NCDOR calculates one portion of a municipality’s distribution according to its “quarterly franchise tax share” and the other portion based upon its “ad valorem share.”193 A municipality’s “quarterly franchise tax share” is equal to the total amount of franchise taxes on electricity that it received in the same related quarter in fiscal year 2013–2014.194 A municipality’s ad valorem share is its “proportionate share” of the amount remaining for distribution after determining each municipality’s quarterly franchise tax share.195 A municipality’s ”proportionate share” is the ratio of ad valorem (property) taxes levied in that municipality to all property taxes levied by municipalities across the state.196 Any municipality that receives a distribution of electricity taxes may spend these revenues for any authorized public purpose.

Telecommunications Taxes

The state has levied a statewide sales tax—at the “combined general rate”197 of 7.0 percent—upon sales of telecommunications services and ancillary services.198 The North Carolina Department of Revenue (NCDOR) collects these taxes and, on a quarterly basis and within seventy-five calendar days of the end of each calendar quarter, distributes a portion of the proceeds of these taxes to municipalities.199 In particular, NCDOR must distribute 18.7 percent of the net proceeds of these taxes less $2,620,948.00.200

The General Assembly enacted a sales tax upon telecommunications services in 2001 to replace a previously applicable gross receipts tax upon telecommunications services.201 A municipality incorporated prior to January 1, 2001, receives a distribution of these taxes based upon its “proportionate share” of the taxes to be distributed to all municipalities incorporated before that date. A municipality’s “proportionate share” is equal to the same percentage share of telephone gross receipts taxes that it received in the same related quarter in which those prior taxes were still in effect.202 A municipality incorporated on or after January 1, 2001, receives a per capita share of the amount to be distributed to all municipalities incorporated on or after this date that is based upon the ratio of its population to the population of all municipalities incorporated on or after this date.203 Any municipality that receives a distribution of telecommunications taxes may spend these revenues for any authorized public purpose.

Piped Natural Gas Taxes

The state has levied a statewide sales tax—at the “combined general rate”204 of 7.0 percent—upon sales of piped natural gas.205 NCDOR collects these taxes and, on a quarterly basis and within seventy-five calendar days of the end of each calendar quarter, distributes a portion of the proceeds of these taxes to municipalities.206 In particular, NCDOR must distribute 20 percent of the net proceeds of these taxes less the cost of administering the distribution.207

NCDOR calculates one portion of a municipality’s distribution according to its “quarterly excise tax share” and the other portion based upon its “ad valorem share.”208 A municipality’s “quarterly excise tax share” is equal to the amount of excise taxes on natural gas that it received in the same related quarter in fiscal year 2013–2014.209 A municipality’s ad valorem share is its “proportionate share” of the amount remaining for distribution after determining each municipality’s quarterly excise tax share.210 A municipality’s “proportionate share” is the ratio of ad valorem (property) taxes levied in that municipality to all property taxes levied by municipalities across the state.211 Municipalities that operated a piped natural gas distribution system as of July 1, 1998, receive an additional distribution.212 Any municipality that receives a distribution of piped natural gas taxes may spend these revenues for any authorized public purpose.

“Powell Bill” Funds (Motor Fuels Tax)

The State of North Carolina levies an excise tax, pursuant to a statutory formula, upon certain types of “motor fuel,” including gasoline.213 In 1951, the North Carolina General Assembly adopted legislation mandating that the state distribute a portion of the proceeds of motor fuel taxes to municipalities to be used for “maintaining, repairing, constructing, reconstructing or widening” any municipally-maintained street.214 The initial, principal sponsor of that legislation in the North Carolina State Senate was Senator Junius K. Powell, and, for that reason, these distributions often are called “Powell Bill” funds.

In 2015, the General Assembly modified the longstanding tie between the state’s motor fuels tax and the amount of street aid distributed to municipalities.215 Now, the General Statutes do not automatically appropriate a certain percentage of the state’s motor fuel tax revenues to municipalities as street aid. Instead, the General Assembly must appropriate moneys on an annual basis to the North Carolina Department of Transportation (NCDOT) for that purpose.216

Even though the funding scheme for municipal street aid has changed, the use of the term “Powell Bill funds” is still widespread. NCDOT distributes yearly appropriations of Powell Bill funds made by the General Assembly according to a two-part formula: three-quarters of the proceeds are distributed among municipalities on a per capita basis, and one-quarter of the proceeds are distributed according to the proportion of miles of public, non-state streets in a given municipality when compared to the miles of such public, non-state streets in all municipalities eligible to receive Powell Bill funds.217

To receive Powell Bill funds, a municipality incorporated after January 1, 1945, must have (1) held the most recent election to elect municipal officials required under its charter or the general law, (2) levied a property tax for the current fiscal year of at least $0.05 per $100.00 in assessed valuation and collected at least 50 percent of the total property tax levy for the previous fiscal year, (3) adopted a budget ordinance in substantial compliance with general law requirements, and (4) appropriated funds for at least two of eight services specified by statute.218 A municipality incorporated after January 1, 2000, must appropriate funds for at least four of those same eight services specified by statute in order to receive Powell Bill funds.219 A municipality incorporated before January 1, 1945, must only demonstrate that it has conducted an election of municipal officers within the preceding four-year period and that it currently imposes a property tax or provides other funds for the general operating expenses of the municipality.220

NCDOT distributes Powell Bill funds to eligible municipalities twice per year—half on or before October 1 and half on or before January 1.221

Permissible Uses of Powell Bill Funds

A municipality that receives Powell Bill funds has three options when expending these moneys.222

The municipality may accept all or a portion of the funds allocated to the municipality for use as authorized by G.S. 136-41.3(a).