County and municipal officials are responsible for acquiring, constructing, and maintaining the facilities, equipment, and other capital assets necessary to perform public services.1 Units of local government in North Carolina perform a wide variety of public services—and as a result, the cost and complexity of the capital assets that a local government might need to perform a given public service (e.g., water and sewer service or operation of a courthouse), can vary substantially according to the types of public services that a unit provides. Because the useful life of a capital asset can extend for multiple fiscal years, the tools that a local government uses to budget for and finance the acquisition or construction of capital projects differ from those used to budget and finance current assets or operating expenses.2

This chapter focuses on funding capital assets used solely or primarily for traditional governmental purposes and explores the five primary mechanisms available to North Carolina’s local governments to finance capital projects: (1) current revenues, (2) savings, (3) special levies, (4) debt, and (5) grants or partnerships.3Table 7.1 lists the authorized financing mechanisms within each category, and the remainder of the chapter details the legal authority of local governments to use each financing mechanism.

Table 7.1 Authorized Capital Financing Mechanisms in North Carolina

Project development financings (tax increment financings)

Leases

Reimbursement agreements

Redevelopment areas

Grants

Gifts/donations/crowd-fundinga

State direct appropriations

a. Crowd-funding involves the use of online platforms to raise private money to fund public infrastructure projects. At its core, crowd-funding simply provides a newer mechanism to accept private donations for specific public improvement projects.

Current Revenues

Current revenues are revenues that a unit of local government collects on a regular, recurring basis (e.g., each fiscal year).4 The largest source of current revenue in a unit’s general fund is typically the property (ad valorem) tax, followed by local sales and use taxes. Current revenues in a unit’s enterprise funds typically encompass user fees and charges.

Although units typically use current revenues to fund government programs and, in particular, to cover recurring operational expenses, including salaries and benefits, utilities, and supplies, many also use a portion of current revenues to fund capital projects. Local governments typically use current revenues to fund two categories of capital expenditures: (1) those falling below a certain dollar amount and (2) those recurring on a regular basis (e.g., maintenance and repair expenditures on capital assets). Some local governments establish in their annual budget ordinance the dollar amount below which they will fund any capital expenditures with current revenues. A particular recurring capital expenditure may exceed that amount, in which case a local government may still choose to finance it using current revenues.

Savings

A unit often must save current revenues over time to finance a capital expenditure. North Carolina’s local governments can do this in two ways: (1) by accumulating moneys in fund balance or (2) by allocating revenues to a capital reserve fund.

Fund Balance

Local governments use fund accounting to track their assets and liabilities.5 In a fund accounting system, each accounting fund contains its own subset of self-balancing accounts—and each fund has its own assets, liabilities, revenues, and expenses.

Several types of funds can exist in a fund accounting system, including a “general fund,” which is both the most common type of fund that local governments hold and which accounts for the majority of revenues and expenditures for general government purposes. Equity within an accounting fund—the difference between its financial assets (e.g., revenues) and liabilities (e.g., expenditures)—is known as “fund balance.”

Primary Purposes

Fund balance serves three primary purposes: (1) to provide sufficient cash flow to cover operating expenses, (2) to serve as an emergency or “rainy day” fund, and (3) to function as a saving mechanism for anticipated capital expenditures.

Covering Operating Expenses

Although the fiscal year for most units of local government and public authorities begins on July 1,6 many local governments do not receive the majority of their current revenues (in the form of property tax proceeds) until late December or early January.7 Therefore, a local government typically must rely upon cash reserves—accumulated in fund balance—from its prior fiscal year to cover expenditures in the first several months of its new fiscal year.

Maintaining an Emergency or “Rainy Day” Fund

Fund balance can also serve as an emergency or “rainy day” fund. In an economic downturn or in response to unexpected expenses (e.g., a natural disaster or pandemic), local governments may have difficulty generating additional revenues (through taxes, fees, or user charges) quickly. Fund balance can provide a local government with cash flow to cover unanticipated operating or capital expenditures.

Saving for Anticipated Capital Expenditures

Some local governments also use fund balance to save money over time for anticipated capital expenditures. For example, if a local government knows that it must finance a capital expenditure in the next several years, it might purposefully enlarge its fund balance in fiscal years preceding the expenditure. When the project begins, the local government can then appropriate moneys accumulated in fund balance to finance the project.

Proper Amounts of Fund Balance

North Carolina law limits the maximum amount of fund balance that a unit may appropriate in an annually budgeted fund, but it does not force units to maintain any minimum level of fund balance. The Local Government Commission (LGC), a division of the North Carolina Department of the State Treasurer responsible for overseeing local government financial-management practices, similarly does not require units to set any minimum amount of fund balance.8 Instead, the LGC has encouraged units of local government to “maintain a fund balance that is consistent with . . . peers that provide similar services”9 and use LGC-published memoranda that list fund balances available for all counties and municipalities10 to determine a unit-specific amount of fund balance to maintain on an annual basis. What may be an appropriate amount of fund balance for one unit (e.g., 8 percent of general expenditures or one month of operating expenditures) may be inappropriate for another.

The LGC recommends that each local government adopt a fund balance policy that can be used to develop operating budgets and provide for corrective action should fund balance drop below the intended level at the close of a fiscal year.11 The LGC also has drafted a sample fund balance policy, which contemplates that certain portions of fund balance “should be contemplated as a funding source for capital needs.”12

Using Savings Held in Fund Balance for Capital Expenditures

Appropriating portions of fund balance for a capital expenditure is relatively simple. A governing board need only amend its budget ordinance or project ordinance to account for and authorize an expenditure for one or more capital projects.13 A governing board may need to take additional actions to authorize a unit to enter into a contract for the acquisition or construction of a capital project.14

Advantages and Disadvantages of Accumulating Savings for Capital Expenditures in Fund Balance

Using fund balance to save money for future capital projects affords flexibility to a local government’s governing board. Because state law does not dictate that a unit spend unrestricted fund balance on a particular project or asset, the board may use the moneys accumulated in fund balance to finance either operating or capital expenditures.15 This flexibility can be beneficial in the face of unexpected events. For example, assume that a county wishes to expand its solid waste disposal facility in approximately five years. The county’s board of commissioners begins to purposefully accumulate fund balance toward this goal, but in year three, the county suffers from an economic recession. In this case, the board may divert the accumulated fund balance—with the exception of any moneys restricted by statute, regulation, or grant condition—to meet unrelated operating expenses or more pressing capital expenditures.

Using fund balance as a mechanism to save for future capital expenditures also may create controversy. Citizens may question why a unit of local government continues to raise revenue (through taxes, fees, and other charges) when it has sufficient reserves to meet its annual cash flow needs. They also may not trust that the governing board ultimately will spend the accumulated fund balance on capital expenditures.

Capital Reserve Funds

Instead of accumulating savings for capital expenditures in fund balance, a unit of local government may establish a capital reserve fund and periodically appropriate money to it.16 North Carolina law enables a unit of local government to establish and maintain a capital reserve fund for any purpose for which it may issue bonds.17 Local government utilities must account for any proceeds of system development fees in a capital reserve fund, regardless of the type of capital projects that the moneys will be used to fund, unless the local government has pledged those revenues as security in a bond financing.18 In that case, the local government may deposit the proceeds of system development fees in the funds, accounts, or subaccounts in accordance with the relevant bond order, bond resolution, trust agreement, or similar instrument that secures the relevant bonds.19

Creating and Amending a Capital Reserve Fund

To create a capital reserve fund, the governing board of a unit of local government must adopt a resolution or ordinance stating:

the purposes for which the capital reserve fund is created,20

the approximate periods of time during which the moneys shall be accumulated in the fund for each purpose,

the approximate amounts to be accumulated for each purpose, and

the sources from which moneys for each purpose will be derived.21

A local government’s governing board may appropriate funds from its annual budget ordinance to a capital reserve fund at any time.22 Whenever it makes an appropriation, the board must amend the capital reserve fund into which the money will be transferred to account for the additional revenue.

The board also can amend a capital reserve fund, at any time, to change the purposes for which the fund was originally created.23 For example, assume that the governing board of a rapidly growing municipality anticipates a need to expand its water system within eight to ten years. The board establishes a capital reserve fund and allocates moneys to the fund on an annual basis for five years for the water-system expansion project. In year six, the municipality suffers from a major economic recession and its growth slows significantly, making a water-system expansion unnecessary. In that case, the governing board can amend the capital reserve fund to identify alternative capital expenditures for which it will expend funds previously accumulated for the water-system expansion (e.g., road improvements, vehicle acquisition, or construction of a new administrative building). The board could not, however, divert accumulated savings in the capital reserve fund to cover the municipality’s operating expenses (e.g., salaries and benefits).

Using Savings Held in a Capital Reserve Fund for Capital Expenditures

Expending moneys held in a capital reserve fund for a capital expenditure is a simple task. The governing board of a unit of local government must adopt an ordinance or resolution authorizing the withdrawal, the transfer of moneys to another fund (e.g., the general fund or an enterprise fund), and the expenditure of moneys for one or more of the capital projects or assets identified in the resolution or ordinance creating the capital reserve fund.24

Advantages and Disadvantages of Accumulating Savings in a Capital Reserve Fund

A capital reserve fund provides a more formal mechanism to save for future capital expenditures than fund balance. A capital reserve fund might be viewed as providing more transparency than an accumulation of fund balance because the governing board of a local unit must specify in the resolution or ordinance creating the capital reserve fund the capital projects for which it will accumulate funds. However, appropriating money to a capital reserve fund also provides a governing board with less flexibility than accumulation of fund balance. Once a governing board appropriates funds to a capital reserve fund, those moneys cannot be used to finance operating expenses—they must be used to fund capital expenditures, even in an emergency or recession.

Special Levies

Units of local government derive most of their current revenues from revenue sources held in the general fund, including the largest revenue source held in the general fund for counties and municipalities: the property (ad valorem) tax.25 Owners of real and personal property subject to ad valorem taxes pay those taxes to a taxing county or municipality without regard to whether they benefit from the services that either jurisdiction provides. Governing boards typically feel obligated to spend the proceeds of property taxes for services that provide general benefits to the community rather than services that offer benefits to a single geographic area or users of a particular public service.

Governing boards also often feel pressure to provide and fund increasing numbers of projects and services while maintaining or reducing the property tax levy. As a result, many counties and municipalities now rely upon mechanisms for targeted revenue generation like user charges or fees, which are paid only by the citizens or property owners that benefit most directly from a service that a county or municipality provides. For example, many municipalities at one time used property tax proceeds to fund solid waste services, including disposal facilities, convenience centers, and even curbside pickup. Now, however, many local governments across the country increasingly assess user fees or charges to cover some or all of the cost to provide these types of services.26

Counties and municipalities commonly impose user fees or charges for wastewater utility services, recreational and cultural activities, health and mental services, ambulance services, parking, public transportation, stormwater, cemeteries, and airport usage. Many counties also rely on fee revenue to fund certain regulatory activities, including inspections and plan reviews.27

User charges are typically an appropriate funding source for services that have specific, identifiable beneficiaries rather than the public at large.28 And although financing capital projects with user charges is possible, it may present challenges. Some units attempt to apportion some of the capital costs associated with providing a particular service among users of that service. For example, a local government that operates a water or sewer system might assess a customer a monthly charge consisting of two components: (1) a variable usage charge that increases or decreases based upon a user’s actual use and (2) a fixed “overhead” charge.29 The fixed “overhead” charge covers both operating overhead and at least some capital expenses.

In addition to user charges, North Carolina law also permits counties and municipalities to use targeted revenue generation to fund capital projects through four types of “special” levies: (1) “traditional” special assessments, (2) critical infrastructure assessments, (3) special taxing districts, and, to a limited extent, (4) development exactions.

Special Assessments

A special assessment is a charge levied against real property to pay for public improvements that benefit that property. It is neither a user charge nor a tax, but shares characteristics of each. Like a user fee, a special assessment is levied in some proportion to the benefit that the assessed property receives. Like a property tax, it is levied against property rather than individuals and creates a lien on each parcel of real property assessed.30

The authority to levy special assessments provides units of local government with a potentially important tool to fund capital projects. Recouping some or all of the costs of a capital project that directly benefits a defined range of property owners can make financial and political sense. Using special assessments to finance public infrastructure projects that primarily benefit a particular set of property owners also can permit a governing board to expend property tax proceeds and other revenue sources in the general fund on projects that benefit a broader subset of a unit’s citizens.

Currently, North Carolina counties and municipalities have two statutory methods for imposing special assessments: (1) “traditional” special assessments and (2) “critical infrastructure” assessments. Using special assessments can permit a unit to recoup some or all of the costs of a particular project.

“Traditional” Special Assessments

North Carolina’s local governments have infrequently imposed “traditional” special assessments for a number of reasons.

First, state law limits the purposes for which counties and municipalities may levy such assessments. Counties may levy assessments to finance water systems, sewage collection and disposal systems, beach erosion control and hurricane protection works, watershed improvement projects, drainage projects, water resources development projects, local costs of N.C. Department of Transportation improvements to subdivision and residential streets located outside of municipalities, and streetlight maintenance.31 Municipalities may levy assessments to finance public improvements involving streets, sidewalks, water systems, sewage collection and disposal systems, storm sewer and drainage systems,32 and beach erosion control and flood and hurricane protection works.33

Second, a county or municipality may pay all the costs of a project prior to levying special assessments. Only after a unit completes a capital project may it levy any special assessments, and assessments often are paid in installments over a number of years (up to ten). Some units have created special assessment revolving funds, using yearly special-assessment payments from former projects to fund the initial costs of new projects.34 But establishing a sufficient revolving fund can take several years.

Third, the process used to levy the assessments—detailed below—is onerous.

Process of Imposing “Traditional” Special Assessments

To impose a “traditional” special assessment, the governing board of a county or municipality must follow the steps in Table 7.2.35

Once a unit confirms the final assessment roll, the assessments become a lien on the real property assessed.36 Although a unit may demand full payment of the assessments within thirty days of publishing the confirmation, it typically permits payment in up to ten yearly installments, with interest.37

Table 7.2 “Traditional” Special Assessment Process

Step

Action Required of Governing Board

1

For street, street light, and sidewalk assessments only—the board must receive a petition from the requisite number of affected property owners.a

2

Adopt a preliminary assessment resolution that includes, among other things, a description and estimated cost of the project, the percentage of the cost to be funded through assessments, the basis of assessments, the terms of payment of the assessments, and the time and place for a public hearing on matters contained in the resolution.b

3

At least ten days prior to the date of the public hearing on the matter, publish notice of adoption of preliminary assessment resolution and the date of the public hearing, and mail a copy of the preliminary resolution to affected property owners.c

4

Hold a public hearing on the preliminary assessment resolution.d

5

Adopt a final assessment resolution setting forth the basis of the assessments, percentage of costs to be funded through assessments, and terms of payment of the assessments.e

6

After completion of the project, determine the project’s total costs.f

7

Prepare preliminary assessment roll, containing a description of each property to be assessed, the amount assessed against each property, the terms of payment, and the name of the owner of each assessed lot. File roll with the clerk to the board and set the time and place for a public hearing on the roll.g

8

At least ten days prior to the date of the public hearing, publish notice of completion of the preliminary assessment roll and state the time and place for the public hearing.h

9

Hold a public hearing on the preliminary assessment roll.i

10

Confirm the assessments, in whole or in part. The clerk to the board must record the date, hour, and minute of confirmation, and, after confirmation, the board must deliver a copy of the confirmation to the county tax collector for collection.j

11

The tax collector must publish the assessment roll no earlier than twenty days from the date of confirmation of the assessment roll.k

a. G.S. 153A-205(c) (streets); 153A-206(d) (street lights); 160A-217(a) (street and sidewalks). Before a county may impose special assessments for street improvements, it must first receive a petition signed by at least 75 percent of the owners of the property to be assessed, who represent at least 75 percent of the lineal feet of frontage of the lands abutting the street or portion of the street to be improved. SeeG.S. 153A-205(c). Similarly, before a municipality may impose special assessments for street or sidewalk improvements, a municipality must receive a petition signed by a majority of the owners of property to be assessed, who represent at least a majority of all the lineal feet of frontage of lands abutting the street or portion of the street to be improved. SeeG.S. 160A-217(a).The General Assembly has modified the petition requirements for certain jurisdictions by local act. See, e.g., S.L. 1989-611, An Act to Revise and Consolidate the Charter of the Town of Wrightsville Beach, § 5.2 (granting authority to assess the costs of sidewalk improvements or repairs without the need for a petition from affected property owners).

e. G.S. 153A-192; 160A-225. State law establishes permissible bases of assessment. SeeG.S. 153A-186; 160A-218. The most common basis of assessment is based upon “front footage”—each property is assessed according to a uniform rate per foot for each foot of property that abuts the project. Other common bases include the size of the area benefited and the value added to each property because of the improvement. All permissible bases of assessment mandate that the assessment basis be made equally across all assessed properties. See G.S. 153A-186; 160A-218.

Beginning in its 2008 legislative session, the General Assembly authorized counties and municipalities to finance a wide range of capital projects through special assessments for “critical infrastructure needs.”38

The authority to impose special assessments for critical infrastructure needs, modeled on similar legislation from other states, can assist counties and municipalities in financing public infrastructure projects that benefit new, private development. A unit may impose assessments, with payments spread out over a period of years, expecting that the ultimate owners of developed property (instead of a private developer or local government) will pay the majority of those costs. Like traditional special assessments, the unit can pay the costs of the project up front and recoup its investment over time through yearly assessment payments. But unlike traditional special assessments, state law permits a unit imposing a critical infrastructure assessment to borrow the initial costs of a project, pledge the assessment revenue as security for the debt that it issues, and use yearly assessment revenues to meet its debt-service obligations.39 Alternatively, a unit may contract with a developer to construct the capital project and use the critical infrastructure assessment revenue to reimburse the developer, over time, for costs that it incurred.40

Capital costs of providing auditoriums, coliseums, arenas, stadiums, civic centers, convention centers, and facilities for exhibitions, athletic and cultural events, shows, and public gatherings

Capital costs of providing hospital facilities; facilities for the provision of public health services; and facilities specially designed for the diagnosis, treatment, education, training, or custodial care of individuals with intellectual or other developmental disabilities

Capital costs of art galleries, museums, art centers, and historic properties

Capital costs of on- and off-street parking and parking facilities, including meters, buildings, garages, driveways, and approaches open to public use

Capital costs of providing certain parks and recreation facilities, including land, athletic fields, parks, playgrounds, recreation centers, shelters, permanent and temporary stands, and lightingb

Capital costs of redevelopment through acquisition and improvement of land for assisting local redevelopment commissions

Capital costs of sanitary sewer systems (including septic systems)

Capital costs of storm sewers and flood-control facilities

Capital costs of water systems, including facilities for supply, storage, treatment, and distribution of water

Capital costs of public transportation facilities, including equipment, buses, railways, ferries, and garages

Capital costs of industrial parks, including land and shell buildings, to provide employment opportunities for citizens of a county or municipality

Capital costs of property to preserve a railroad corridor

Capital costs of providing community college facilities

Capital costs of providing school facilities

Capital costs of improvements to subdivision and residential streets, in accordance with G.S. 153A-205

To finance housing projects for persons of low or moderate income

Capital costs of electric systems

Capital costs of gas systems

Capital costs of streets and sidewalks (including traffic controls and lighting)

Capital costs of improving existing systems or facilities for transmission or distribution of telephone services

Capital costs of housing projects for persons of low or moderate income

To provide or maintain beach erosion control and flood and hurricane protection works, downtown revitalization projects, urban area revitalization projects, transit-oriented development projects, drainage projects, sewage collection and disposal systems, off-street parking facilities, watershed improvement projects, water resources development projects, and conversions of private residential streets to public streetsc

Installation of distributed-generation renewable energy sources or energy-efficiency improvements that are permanently fixed to residential, commercial, industrial, or other real propertyd

a. Counties and municipalities may impose critical infrastructure assessments to assist in the arranging for payment of the capital costs of projects (1) for which project-development-financing debt instruments may be issued under G.S. 159-103 and (2) for the purpose of the installation of distributed-generation renewable energy sources or energy-efficiency improvements that are permanently fixed to residential, commercial, industrial, or other real property. SeeG.S. 153A-210.2(a); 160A-239.2(a). Items 1 through 23 list the projects for which project-development-financing debt instruments may be issued. Through July 1, 2022, counties had authority under general law to make critical-infrastructure assessments for certain dam repair projects. SeeG.S. 153A-210.2(a1); S.L. 2019-190, § 2. Due to statutory conditions limiting the dam repair to only certain types of dams, only two counties—Richmond and Moore—were likely to exercise this authority. SeeNicholas Giddings, Staff Attorney, N.C. General Assembly Legislative Analysis Division, Analysis of Second Edition of Senate Bill 190: Expand Special Assessments for Dam Repair (June 18, 2019). As of March 1, 2023, the General Assembly has not extended the authority to impose special assessments for dam repair projects. SeeG.S. 153A-210.2(b).

b. G.S. 159-103(a) does not permit the issuance of project-development-financing debt instruments for certain types of parks and recreation facilities: stadiums, arenas, golf courses, swimming pools, wading pools, and marinas. Therefore, counties and municipalities may not impose critical-infrastructure assessments to pay for the cost of these parks and recreation facilities.

c. Counties may impose critical-infrastructure assessments to assist in the arranging for payment of the capital costs of projects for which project-development-financing debt instruments may be issued under G.S. 159-103. SeeG.S. 153A-210.2(a). G.S. 159-103 permits the issuance of project-development-financing instruments and the use of resulting proceeds for, among other things, “any service or facility authorized by G.S. 160A-536 to be provided in a municipal service district.” G.S. 159-103(a). Counties and municipalities each have authority to create and maintain, respectively, county and municipal service districts for (1) beach erosion control and flood and hurricane protection works; (2) sewage collection and disposal systems of all types, including septic tank systems or other on-site collection or disposal facilities or systems; and (3) watershed improvement projects, drainage projects, and water-resources development projects. SeeG.S. 153A-301(a)(1), (4), (8); 160A-536(a)(1), (3), (3a), (5). However, counties lack explicit authority to provide services or facilities for five purposes listed in G.S. 160A-536: (1) downtown revitalization projects, (2) urban area revitalization projects, (3) transit-oriented development projects, (4) off-street parking facilities, and (5) conversion of private residential streets to public streets. SeeG.S. 160A-536. Even assuming that counties have authority to issue project-development-financing debt instruments under G.S. 159-103(a) and thus impose critical-infrastructure assessments for these purposes under G.S. 153A-210.2(a), it is not clear that counties have underlying authority to carry out these functions listed in G.S. 160A-536.

d. Note that G.S. 160D-1320(b) authorizes local governments to establish programs to finance the purchase and installation of distributed-generation renewable energy sources or energy-efficiency improvements that are permanently affixed to residential, commercial, industrial, or other real property. These statutes authorize a local government to (1) purchase the renewable energy sources or energy-efficiency improvements and install them on private property or (2) contract for their purchase or installation. Renewable energy sources include “solar electric, solar thermal, wind, hydropower, geothermal, or ocean current or wave energy resource; a biomass resource, including agricultural waste, animal waste, wood waste, spent pulping liquors, combustible residues, combustible liquids, combustible gases, energy crops, or landfill methane; waste heat derived from a renewable energy resource and used to produce electricity or useful, measurable thermal energy at a retail electric customer’s facility; or hydrogen derived from a renewable energy resource.” SeeG.S. 160D-1320(c) (noting that “renewable energy source” has the same meaning as “renewable energy resource in G.S. 62-133.8); 62-133.8(a)(8) (defining “renewable energy resources”). The term does not include peat, a fossil fuel, or a nuclear energy resource.” Id. The General Statutes do not define “energy efficiency improvements.”

A critical-infrastructure assessment is conceptually similar to an “impact fee.” An impact fee is a fee that a unit of local government levies on new development (typically as a condition of obtaining a building permit) to pay for public infrastructure costs that the new development imposes.41 Like it may with an impact fee, a municipality or county may use the proceeds of critical-infrastructure assessments to fund public infrastructure projects that new private development requires—but the critical-infrastructure assessment method typically imposes fewer costs on a developer than an impact fee does. Assuming the developer completes the project, many, if not most, of the payments will be collected after completion.

Counties and municipalities may finance a much broader array of public infrastructure projects through critical-infrastructure assessments than through traditional special assessments. Authorized projects include a variety of traditionally “public” projects, ranging from constructing and maintaining public roads to building public schools, and encompass most capital projects in which a county or municipality is authorized to engage.42 The sidebar above presents a list of authorized critical-infrastructure projects.

Advantages and Disadvantages of “Critical Infrastructure” Assessment Method

A unit may use critical-infrastructure assessment revenues to make its debt-service payments and pledge those assessment revenues to debt holders to secure the debt that it incurred. Therefore, unlike traditional special assessments, critical-infrastructure assessments allow counties and municipalities to borrow money to cover the cost of an authorized capital project without committing general fund revenues to the project.

Of course, a unit may not be able to collect all of the assessment revenues necessary to meet its debt-service obligations. However, a unit can use the remedies available for the collection of property taxes in collecting unpaid assessments. In fact, the trust agreement under which a county or municipality issues special assessment–backed debt likely will include a covenant requiring the unit to use similar policy and effort in collecting special assessments as it does for property taxes.43

Even though counties and municipalities have robust authority to collect unpaid special assessments, debt backed by special assessments can pose more risk to investors than other types of local government debt (e.g., general obligation bonds). To compensate investors for this risk, special assessment–backed debt typically carries higher rates of interest than other types of borrowing.44

Process of Imposing “Critical Infrastructure” Assessments

With some exceptions, the process of imposing “critical infrastructure” assessments is similar to the process of imposing “traditional” special assessments as detailed in Table 7.2.

Table 7.3 summarizes the major differences between the two methods of imposition. Of particular note, before a county or municipality may impose any critical infrastructure assessment, it must first receive a petition signed by a majority of the owners of real property to be assessed, whose real property also represents at least 66 percent of the assessed value of all real property to be assessed.45 In setting this requirement, the General Assembly likely envisioned that a single or just a few individuals or entities (e.g., corporate developers) would own the subject properties at the time of assessment. The petition must include a description of the public infrastructure projects to be financed, their estimated costs, and an estimate of the percentage of estimated costs to be assessed.46 A developer owning real property to be assessed would likely negotiate all of these points with a county or municipality prior to submitting a petition. Once a county or municipality receives a petition to impose a critical-infrastructure assessment, it generally must follow the same detailed statutory process to impose the assessments as is required for traditional special assessments.

Table 7.3 Comparison of Authorized Special-Assessment Methods

Traditional Special-Assessment Method

Critical-Infrastructure Assessment Method

Limited statutory purposes

Generally, no petition requirement (except for street and sidewalk projects)

Amount of assessment must be based on one or more statutory bases

Unit must follow detailed statutory procedures before levying assessments (including at least two public hearings)

Unit may borrow money to front costs of a project funded with assessments but may not pledge assessment revenue as security for debt issued

Unit must complete public improvement project before imposing assessments

Assessments may be paid in up to ten yearly installments

Statutory authority does not contain a sunset date

Expansive statutory purposes

Petition requirement for all projects

Assessment method within discretion of governing board but must relate to benefit to properties assessed

Unit must follow detailed statutory procedures before levying assessments (including at least two public hearings)

Unit may borrow money to front costs of a project funded with assessments and may pledge the assessments as security for debt issued

Unit may impose assessments before the project is complete, based on estimated costs

Assessments may be paid in up to twenty-five yearly installments

Statutory authority expires July 1, 2025, for projects that have not been approved under a final assessment resolution

Unlike traditional special assessments, for critical-infrastructure assessments a unit need not complete a project before confirming the final assessment roll. Instead, it may base its assessments upon an estimate of the total costs to perform the project.47 A unit also is not limited to a ten-year repayment period as it is when imposing traditional special assessments. It can instead set a repayment period of up to twenty-five years.48

Frequency of Use Since Initial Authorization

To date, only two units of local government—the Town of Hillsborough and the Town of Mooresville—have issued debt backed by critical-infrastructure assessments.49 Similar mechanisms are used more frequently in other states, particularly in Florida, Georgia, and Texas.50

Special Taxing Districts

A municipality or county might fund a capital project using targeted revenue generation by establishing a special taxing district. Although the North Carolina Constitution requires that a local government’s rates of property tax be uniform throughout the jurisdiction,51 it also authorizes the General Assembly to permit counties and municipalities to (1) delineate one or more geographic areas within the unit as special taxing districts and (2) levy taxes within those districts to finance or provide services or facilities to a greater extent than those financed or provided in other parts of the jurisdiction.52 The General Assembly has exercised that authority in several cases, most notably in authorizing counties and municipalities to create “service districts.”53

Like special assessments, these special taxing districts are based upon the principle that those benefitting most directly from a government function should pay for it. But unlike special assessments, which must be assessed on a project-specific basis, a county or municipality can establish a special taxing district to fund a variety of projects or services benefitting properties in the district on an ongoing basis. Chapter 4, “Revenue Sources,” details what types of service districts counties and municipalities may establish, the process to establish a service district, municipal and county authority to levy taxes in service districts, and what types of projects a county or municipality may undertake in a service district.

A county or municipality may borrow money to fund capital projects located in a service district to the same extent, and in the same manner, as it funds similar capital projects located outside of a service district. In addition, a municipality may issue special obligation bonds to finance capital projects located in a municipal service district.54

Counties and municipalities typically are subject to an additional procedural requirement when issuing general obligation (GO) bonds to fund capital projects in service districts. If the GO bonds are subject to voter referendum, a majority of the district’s voters must approve the issuance of bonds, in addition to a majority of the voters residing within the municipality or county.55

Development Exactions

Local governments sometimes seek to impose development exactions to finance the cost of public infrastructure projects. Exactions typically take one of two forms: (1) a requirement that a developer compensate a unit of local government for the capital costs the unit incurred to acquire or construct public infrastructure that supports the development or (2) a requirement that a developer construct public infrastructure to support its development. Local governments in North Carolina have limited statutory authority to impose development exactions.56

Borrowing Money

The most common method for financing costly capital projects is borrowing money. Neither current revenues nor savings or special levies are likely to generate sufficient revenues to finance the acquisition, construction, or equipping of a significant capital asset. Borrowing money allows a unit of local government to leverage future revenue streams—a unit obtains cash in the short term and uses future revenues to repay debt over time.

When a unit of local government borrows money, it agrees by contract—typically referred to as a “debt instrument”—to repay those that have loaned money to it. Should a local government breach its promise to repay its debt or any other promise it makes under the terms of the debt instrument, its lenders typically have legal rights to enforce repayment or force the unit to cure its default.

Debt instruments can take a variety of legal forms, but most commonly take the form of a bond. North Carolina’s local governments are authorized to issue general obligation bonds, revenue bonds, special obligation bonds, project-development-financing bonds, and limited obligation bonds. North Carolina local governments also may borrow money through installment financing contracts. This section addresses each of these mechanisms for issuing debt.

Security

When a local government borrows money, its most fundamental promise is to repay the debt it incurs. But in addition, a local government also may pledge to its lenders certain legal rights to force or “secure” the repayment of its debt. Those legal rights are known as “security.” Depending on the type of transaction, that security might take the form of, among other things, a right to force a defaulting local government to levy taxes to repay its debt, to require changes in the operation of a public enterprise that the local government operates, or to repossess certain property that the defaulting local government owns.

North Carolina law dictates what types of security a local government may pledge to its lenders in connection with each authorized method of borrowing. The type of security that a local government pledges can affect the form of debt instrument issued, whether a unit must obtain voter approval or approval from the Local Government Commission (LGC), and the cost of debt.

For each borrowing mechanism, Table 7.4 explains (1) the “primary” sources of security—those that a local government legally may and typically does pledge to its lenders and (2) the “secondary” sources of security—those that a local government sometimes, but less commonly, pledges in order to make a financing more attractive for lenders. The primary sources of security for each borrowing mechanism are discussed below.

Table 7.4 Authorized Securities for Borrowing Transactions

Primary Security

Authorized Secondary Securities

General Obligation Bonds

Full faith and credit (taxing power)

Revenues generated by revenue-generating asset or system

Revenue Bonds

Revenues generated by revenue-generating asset or system

Critical-infrastructure assessments

Asset(s) or part of asset(s) being financed

Special Obligation Bonds

Any unrestricted revenues other than unit-levied taxes

Asset(s) or part of asset(s) being financed

Project-Development-Financing Bonds

Incremental increase in property tax revenue within defined area due to new private development

Asset(s) or part of asset(s) being financed

Any unrestricted revenues other than unit-levied taxes

Special assessments

Installment Financings

Asset(s) or part of asset(s) being financed

Entities Involved

Borrowing money often requires a unit of local government to interact with a range of third parties. These outside entities might include bond counsel, financial advisors, underwriters, lenders, ratings agencies, trustees, and the LGC. Not all of these parties are involved in every borrowing, and local governments often complete simple, small borrowings without external guidance or oversight.

Bond Counsel

A private law firm acts as “bond counsel.” When a local government issues bonds, the primary duty of bond counsel is to render a legal opinion that addresses, among other things, (1) the validity of bonds that a local government issues and (2) the taxability of interest paid to holders of the bonds under federal and state income tax laws.57 Local governments and the purchasers of their bonds typically require receipt of this legal opinion as a condition of closing a bond transaction. Prior to issuing its legal opinion, bond counsel guides a local government—in concert with a unit’s regular attorney—through the procedural steps required to issue debt under state law. Bond counsel also prepares the majority of the legal documents required to complete a bond issuance. Through its involvement throughout this process, bond counsel is able to provide its approving legal opinion when a transaction is completed.

After an issuance occurs, bond counsel also might advise a local government about how to comply with complex provisions in the federal tax code that regulate how a unit may spend or invest proceeds of “tax-exempt” bonds.58 Bond counsel also might advise a local government about its obligations under federal securities laws to disclose certain facts affecting bonds issued or the local government’s financial condition.59 The terms of an engagement letter between a unit of local government and a private law firm providing bond counsel services will dictate whether and at what expense these services will be provided.

If a unit of local government is contemplating a bond issuance, it should hire reputable bond counsel with prior experience advising a North Carolina local government in the issuance of debt.60 In doing so, a unit should seek to understand the specific functions that bond counsel will perform during the initial issuance of the bonds and after the debt has been issued.

Financial Advisor

Although no law requires a local government to hire a private firm to advise it or advocate for its interests when issuing debt, many local governments hire private firms as financial advisors to assist with the structuring and sale of bonds. These financial advisors might analyze, among other things, a local government’s ability to add additional debt, its compliance with existing debt covenants, or the proper mechanism to finance a new capital project. A financial advisor that advises a local government in connection with the issuance of its debt—including advice with respect to the structure, timing, and similar matters of debt—must register as a “municipal advisor” with the federal Securities and Exchange Commission.61 “Municipal advisors” have fiduciary duties under federal law to act in the best interests of their clients.62

A local government can engage a municipal advisor for a single debt issuance or for a range of services that extend beyond a particular transaction.63 The staff of the Local Government Commission can and will assist a local government in considering the structure of its debt or the proper mechanism for financing a project, but unlike a private “municipal advisor,” these staff may assist in the Commission’s decisions to approve or deny a particular debt issuance.

Other Consultants

A local government may need to hire other consultants to complete certain types of bond issuances. In particular, a local government that issues revenue bonds—which are payable from the proceeds of certain revenue-generating assets (e.g., municipally owned water and sewer systems)—might hire a “financial feasibility consultant.” Such a consultant might produce a “financial feasibility report,” which projects the operating results of the revenue-generating assets securing the repayment of the bonds. The intent of this report is to demonstrate to potential investors that a local government will be able to service its debt and comply with certain financial covenants after issuing revenue-backed debt.64

Underwriter or Lender

An underwriter is a financial institution that purchases an issue of local government debt for resale to institutional or individual investors. An underwriter may initially acquire bonds either by (1) competitive sale or (2) negotiation with a borrowing unit.

Most general obligation bond sales in North Carolina are conducted on a competitive basis; underwriters submit sealed bids to the Local Government Commission (LGC) to buy the bonds, and the LGC awards the sale to the firm providing the most favorable offer.65 Other types of bond sales (revenue bonds, special obligation bonds, project-development-financing bonds, and limited obligation bonds) occur by negotiation.66 In a negotiated sale, a local government selects one or more underwriters at the outset of a transaction and negotiates the financing structure and borrowing costs with the selected firm.67

Underwriters that purchase and resell a local government’s bonds to investors must comply with certain federal securities regulations, including the SEC’s “Rule 15c2-12.”68 With some exceptions, these underwriters must (1) obtain certain disclosure documents from the local government that describe the bonds to be sold and certain information about the issuer of the bonds, (2) distribute these disclosure documents to potential investors, and (3) reasonably determine that the issuer has agreed to provide continuing disclosure of certain information after the bonds are issued.69 An underwriter typically hires legal counsel to advise it on the structure of the offering and its responsibilities, and a local government typically pays for the cost of such legal counsel at closing out of bond proceeds.

In some cases, a financial institution may not purchase a local government’s bond or debt in order to resell it to other investors. Instead, it may hold this debt on its own balance sheet. A financial institution participating in such a “private placement” may be referred to as a “lender” rather than an “underwriter.”

Rating Agencies

A “public offering” occurs when a unit of local government sells bonds to an underwriter that will be offered publicly (i.e., resold to individual and institutional investors). As a practical matter, bonds that are sold publicly must be rated.70 At present, three nationally recognized credit rating agencies rate local government debt: Moody’s Investors Service, S&P Global Ratings, and Fitch Ratings. A bond’s rating can serve as an indication of its credit risk at a given point in time, and each credit agency has a slightly different methodology of determining a credit rating.71

A local government typically will submit a wide variety of information to a rating agency in order to receive a credit rating for a particular public offering of bonds. These disclosures can vary substantially but typically include information regarding the particular debt structure proposed; the unit’s financial condition, demographics, and management practices; and, if applicable, the revenue sources supporting the issuance of the bonds.

Trustee

A trustee is a corporate entity—typically an arm of a financial institution—that is involved in some, but not all, issuances of local government debt.72 Subject to the terms of the bond documents under which bonds are issued, a bond trustee usually takes several actions throughout the life of a bond. It might act on behalf of bondholders in the event a local government defaults under the terms of the bond documents, obtain certain disclosures from the local government over the life of the bonds, and, as a “paying agent,” collect a local government’s payments of principal and interest and ensure their proper application.73

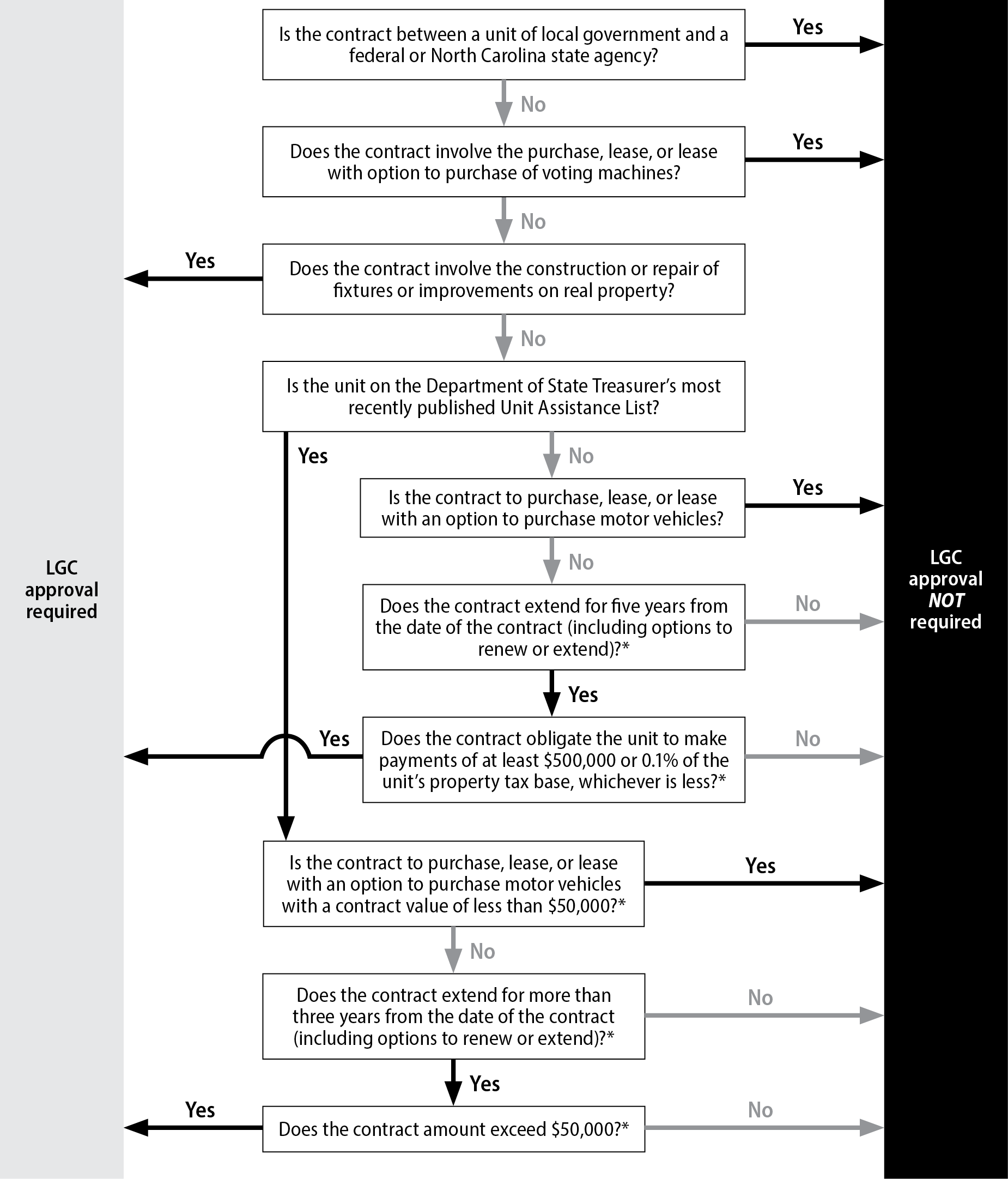

Local Government Commission

The Local Government Commission (LGC), a division of the North Carolina Department of State Treasurer, is a nine-member body responsible for fiscal oversight of local governments and public authorities in North Carolina.74 The LGC must approve each new issue of general obligation bonds, revenue bonds, special obligation bonds, and project-development-financing bonds.75 It also must approve some installment financings, certain leases, and other financial agreements.76

In reviewing proposed issuances of debt, state law requires the LGC to consider certain criteria specified by statute that vary between different types of borrowing. Generally, the LGC must determine whether, considering its other debts, a unit can afford to borrow a proposed amount at a particular rate of interest.

The staff of the LGC will work with a unit throughout the borrowing process to help its officials determine the most advantageous borrowing method for a proposed project. The staff can also identify any deficiencies in the unit’s financial history or management practices that might prevent LGC approval. When contemplating an issuance of debt that will require LGC approval, local officials should contact LGC staff as early as possible for assistance (preferably after the initial scope of a capital project is determined).77

Joint Legislative Committee on Local Government

In 2011, the General Assembly established the Joint Legislative Committee on Local Government as a legislative study committee.78 The purpose of the committee is, among other things, to “review and monitor” local government capital projects (other than those relating to schools, jails, courthouses, or administrative buildings) that require both LGC approval and the issuance of local government debt exceeding $1 million.79 The committee may only review and monitor capital projects—it has no authority to approve or reject a capital project or financing.

Any unit of local government embarking upon a capital project within the legislative committee’s purview (i.e., those that require both LGC approval and the issuance of debt exceeding $1 million) must submit a letter to the chairs of the committee, its assistant, and the Fiscal Research Division of the General Assembly at least forty-five days prior to the meeting at which the LGC will consider approval of the debt.80 The letter must include (1) a description of the project, (2) the debt requirements of the project, (3) the means of financing the project, and (4) the source or sources of repayment for project costs.81 The LGC has encouraged units to consult their regular counsel or bond counsel when preparing this letter.82

The committee may meet at the discretion of its co-chairs to review a proposed capital project83 and may send a letter of objection or support to the LGC for a particular project. In addition, the committee may make periodic reports on local government capital projects that it reviews and also recommend that the General Assembly adopt legislation relating to local government borrowing authority.84

Types of Authorized Borrowing

The General Assembly may only authorize units of local government to borrow money by general law—not by local act.85 At present, North Carolina’s local governments may issue seven types of debt: (1) general obligation bonds, (2) revenue bonds, (3) special obligation bonds, (4) project-development-financing instruments, (5) bond anticipation notes, (6) installment financing contracts or limited obligation bonds, and (7) bonds or notes issued to the federal or state government to repay a loan from an agency of either entity.86 The General Assembly also has bestowed borrowing authority upon certain types of public authorities.87 Summaries of each debt mechanism follow.

General Obligation Bonds

Security and Authority

The strongest form of security that a county or municipality can pledge to secure the repayment of its debt is its “full faith and credit.” When a unit of local government makes such a pledge, it promises to take all actions within its power—including levying property taxes in any amount necessary—to repay the debt. Such a pledge creates a “general obligation” of the unit. For that reason, debt secured by a general obligation is called a “general obligation bond.”

The Local Government Bond Act is the primary source of authority for units of local government to issue general obligation (GO) bonds.88 The Act specifies the types of capital projects that a county or municipality may fund with the proceeds of GO bonds.89 Counties and municipalities can use the proceeds of GO bonds to finance most of the capital projects in which they are otherwise authorized to engage.

Requirements and Limitations

Although North Carolina law authorizes units of local government to issue GO debt for a wide variety of purposes, the process it imposes to issue such debt limits its practical importance. Prior to issuing a GO bond, a unit of local government typically must (1) hold a successful voter referendum before pledging its faith and credit, (2) ensure that a borrowing not exceed its “net debt” limit, and (3) obtain approval from the Local Government Commission.

Voter Approval Requirements

Except in limited circumstances, a unit of local government may not issue GO bonds unless a majority of its voters voting in a referendum approve such an issuance.90 Voters participating in a referendum may be unlikely to support the issuance of GO bonds to finance controversial or less-popular projects (e.g., jails or landfills), and local governments often exercise caution when proposing the issuance of GO bonds to voters. Even referenda for popular projects, such as a park, can fail. For example, from November 2012 through November 2022, six of the eleven GO bond referenda that failed across the state were to finance parks and recreation projects.91

From November 2012 through November 2022, North Carolina voters approved 202 of 213, or 94.8 percent, of GO bond referenda.92 Although this high approval rate suggests that securing voter approval of a proposed GO bond issuance can generally be expected, it also suggests that local governments do not proceed with the lengthy process of issuing GO bonds and securing voter approval for projects expected to be controversial or unpopular in the community. Units of local government often use other borrowing mechanisms authorized under state law—for which no voter approval is required—to avoid the time and expense incurred in securing voter approval for a GO bond issuance.

Exceptions to the Voter Approval Requirement for General Obligation Bonds

A municipality or county need not obtain voter approval to issue certain types of GO bonds. In particular, as permitted by the North Carolina Constitution, the General Assembly has permitted the issuance of “refunding” bonds and “two-thirds” bonds without voter approval.93

Refunding Bonds

A unit of local government issues refunding bonds to retire or “pay off” an existing debt. Most commonly, a unit will issue refunding bonds because interest rates have fallen and, as a result, the unit can issue debt at an interest rate lower than that of the debt to be paid off. If this is the case, a unit can lower its debt-service payments by issuing refunding bonds. Under North Carolina law, a unit need not obtain voter approval to issue GO refunding bonds.94

Municipal bond investors often seek to prohibit bond issuers from paying off existing bonds prior to their maturity date (i.e., the date upon which an issuer must pay all remaining principal and interest on a bond).95 Therefore, GO bonds often include provisions that prohibit the early retirement—known as the “call”—of a bond issue for a certain period of time (typically ten years).96

In some cases, bond issuers can still take advantage of falling interest rates prior to the “call” date of a bond by using a mechanism known as “advance refunding.” In an advance refunding, a unit issues refunding bonds but, instead of using the proceeds of the refunding bonds to immediately retire the outstanding obligations, places proceeds in an escrow account controlled by an independent third-party (most commonly, a trustee). The trustee invests the proceeds of the refunding bonds, makes payments to the holders of the refunded bonds in accordance with the payment schedule for those refunded bonds, and retires (i.e., pays off) the remaining principal and interest on the refunded bonds on or after their call date.

Recent changes in federal income tax laws have decreased the usefulness of advance refunding. Prior to January 1, 2018, interest paid to holders of refunding bonds was exempt from federal income tax as long as the refunding bonds were issued at least ninety days prior to the call date of refunded bonds. In December 2017, Congress repealed that exemption for refunding bonds issued after January 1, 2018—making interest paid on refunding bonds federally taxable.97 To compensate for the loss of the tax exemption, issuers must pay relatively higher rates of interest to holders of advance refunding bonds issued after January 1, 2018.98

A local government interested in retiring debt prior to its maturity date should consult bond counsel to determine what options might exist for refinancing.

Two-Thirds Bonds

A unit of local government need not obtain voter approval to issue GO bonds in an amount equal to or less than two-thirds of the amount by which the unit reduced its outstanding indebtedness in the immediately preceding fiscal year.99 A unit may only issue these types of GO bonds—known as “two-thirds bonds”—in the fiscal year immediately following the year in which it reduced its debt.

A unit’s reduction in outstanding indebtedness is determined only by reference to its net reduction in the amount of outstanding principal in a prior fiscal year—not by any interest that the unit pays. If a unit issues debt in a prior year, it may increase its overall outstanding indebtedness and therefore lack any ability to issue two-thirds bonds in a subsequent fiscal year.

With several exceptions, a unit may use non-voted two-thirds bonds for any purposes authorized by general law.100 When the governing board of a county or municipality announces its intention to issue two-thirds bonds without securing voter approval, the unit’s citizens can force a referendum by submitting to the unit’s clerk a petition signed by at least 10 percent of the unit’s registered voters.101

Net-Debt Limitation

A unit may not issue general obligation (GO) bonds if the issuance would raise the “net debt” of a unit to 8 percent of the aggregate appraised value of property subject to taxation by the unit.102 The General Statutes prescribe a formula for calculating a unit’s “net debt,” which is reflected in Figure 7.1.103 A county or municipality is likely to repay GO and installment financing debt with the proceeds of property taxes—and this limitation seeks to ensure that a unit has sufficient taxing capacity to support the debt incurred.

For many units, this “net debt” limitation is more theoretical in its limitation than practical.104 However, some units set a target net-debt threshold in order to bolster their credit ratings.

Bond Issuance Process

The process to issue GO bonds that require voter approval is long and requires detailed planning and coordination among a unit’s staff, bond counsel, the Local Government Commission (LGC), and other third parties (e.g., financial advisors or ratings agencies).105 Bond counsel typically assists a unit’s staff in the preparation of public notices, required statements that a finance officer must prepare or file, and documents to be approved by the governing board and the LGC. The LGC must approve all issuances of GO bonds—even those that do not require voter approval.106

LGC Approval

State law prescribes an application process for units to follow when seeking the LGC’s approval of a GO bond issuance. But even prior to that formal process, the LGC’s staff—in particular, employees of the Local Debt Management Section of the North Carolina Department of State Treasurer’s State and Local Government Finance Division—can meet with a unit’s representatives to discuss plans for a bond issuance.107

Application Process

To initiate the application process, a unit must file with the LGC an application for the approval of a GO bonds issuance.108 The LGC may require the unit’s staff to meet with LGC staff prior to the acceptance of the application.109

Adoption of Bond Order

After the LGC accepts the unit’s application, the governing board of the unit must adopt a “bond order,” which is the central document the governing board must approve prior to issuing a GO bond.110 Among other things, a bond order authorizes the issuance of the bond and states both the purpose for which the unit will spend the proceeds of the bond and the maximum amount of bonds that may be issued under the bond order.111 If a unit proposes to issue GO bonds for unrelated purposes (e.g., schools and public parks), it must adopt a separate bond order for each purpose.112 Bond orders authorizing the issuance of bonds for which voter approval is required do not take effect unless and until the voters approve them.113

Preparation of Sworn Statement of Debt and Statement of Disclosures Necessary for Bond Authorization

After a unit’s governing board has introduced a bond order authorizing the issuance of GO bonds, the unit’s finance officer must prepare and file with the clerk to the governing board a sworn statement of debt.114 This statement reflects the unit’s net debt, the assessed value of property subject to taxation by the unit, and the percentage of net debt compared to that assessed value.115 As discussed previously, that percentage may not exceed 8 percent.

As of October 1, 2022, the finance officer of a unit intending to issue GO bonds also must file a statement of disclosure with the LGC and the clerk to the governing board that contains (1) an estimate of the total amount of interest that will be paid on the bonds over their expected term, if issued, and a summary of the assumptions upon which that estimate is based; (2) an estimate of the increase in property tax rate, if any, necessary to service the proposed debt; and (3) the amount of two-thirds bonds capacity the unit has available for the current fiscal year.116

LGC Approval Criteria

North Carolina law requires the LGC to approve a debt issuance if it finds and determines all of the following:

The proposed bond issue is necessary or expedient.

The amount proposed is adequate and not excessive for the proposed purpose of the issue.

The unit’s debt-management procedures and policies are good or reasonable assurances have been given that its debt will henceforth be managed in strict compliance with law.

The increase in taxes, if any, necessary to service the proposed debt will not be excessive.

The proposed bonds can be marketed at reasonable rates of interest.

The assumptions used by the unit’s finance officer in preparing the “statement of estimated interest” are reasonable.117

In November 2022, the LGC adopted a “safe harbor policy” to govern its assessment that a unit’s finance officer used reasonable assumptions in the statement of disclosure when determining the total interest to be paid over the expected term of the bonds. Under that policy, the LGC will find such assumptions to be reasonable if they assume that (1) principal will be paid in twenty annual equal principal installments and (2) the interest rate on the bonds will be equal to a Bond Buyer 20 index (BB20) rate published within twenty-five days prior to the introduction of the bond order plus 200 basis points (2 percent) or higher.118

Voter Approval and Issuance of the Bonds

The governing board of a unit of local government must call for a referendum on the bonds to be held within one year after the bond order’s passage.119 After the bond order is approved by voters, the unit may issue bonds authorized under the bond order within seven years of the date upon which the bond order takes effect.120 After the unit adopts a resolution fixing the details of bonds to be issued,121 the LGC sells GO bonds on behalf of the unit, typically on a competitive basis.122

Revenue Bonds

Security and Authority

The State and Local Government Revenue Bond Act authorizes certain units of local government to issue “revenue bonds.”123 Local governments issue revenue bonds to finance the acquisition, construction, or equipping of a single revenue-generating asset (e.g., a parking deck) or multiple assets contained within a revenue-generating system (e.g., water and sewer lines in a portion of a municipality’s water and sewer system). Although North Carolina’s local governments most commonly issue revenue bonds to finance water- and sewer-system projects, they also have legal authority to issue revenue bonds for gas or electric facilities, solid waste facilities, parking, marine facilities, auditoriums, convention centers, economic development, electric facilities, public transportation, airports, hospitals, stadiums, recreation facilities, and stormwater drainage.124

When a local government issues revenue bonds, its obligation to repay the proceeds of those bonds is secured by a “pledge” of the revenue generated by the financed asset (e.g., a parking deck) or system of which the debt-financed asset becomes a part (e.g., a municipal water and sewer system). By law, holders of these revenue bonds have a lien on these pledged revenues,125 and typically, if a local government fails to pay principal and interest upon the bonds as each becomes due, these bondholders can demand that a local government raise its rates or change the operations of its revenue-generating system in order to pay the debt service owed.

North Carolina law only allows units of local government to pay debt service on revenue bonds from revenues pledged as security for the bonds.126 For example, a municipality that issues revenue bonds to finance the construction of a public parking deck may only use revenues generated by its operation of that parking deck (e.g., parking fees) to pay principal and interest to revenue bondholders. In most cases, holders of revenue bonds do not have a right to demand that a local government raise taxes or demand payment from any source other than the revenues of the financed asset or system.127

Requirements and Limitations

Covenants

Because the revenues of an asset or system financed with revenue bonds both secure and serve as the source of repayment for revenue bonds, lenders and underwriters that resell bonds to investors typically require that revenue bond issuers agree to abide by certain restrictions when operating financed assets. These restrictions are known as “covenants.”128

Although the exact form of covenants will vary by transaction, almost all issuers of revenue bonds can expect to make a “rate covenant.” Under a rate covenant, an issuer of revenue bonds typically agrees to set and collect the rates, fees, and charges of revenue-producing assets to ensure that the assets’ net revenues exceed annual debt-service requirements by a certain percentage.129 For example, an issuer will commonly agree to ensure that its rates and charges will generate annual net revenues of between 120 and 150 percent of either the current year’s debt-service requirements or the maximum annual debt-service requirements during the life of the loan.130 This margin of safety is referred to as “times-coverage” or a “debt service coverage ratio” and serves as a measure of the issuer to repay its debt without excess financial strain.131 If an issuer fails to meet its debt-service coverage ratio, bondholders may have certain rights to force the issuer to change the operations of the financed assets.

Issuers of revenue bonds also typically agree to certain restrictions on their ability to issue additional revenue bonds that are secured and payable from the same source of revenues as previously issued bonds.132 Known as an “additional bonds test,” this covenant generally permits an issuer of revenue bonds to issue additional bonds that are secured by and payable from the same source of revenues as outstanding revenue bonds only if the issuer can demonstrate that the net revenues have been and will continue to be sufficient to service the additional debt.

Lastly, revenue bond issuers also commonly agree to maintain various funds (e.g., a revenue fund, a debt-service fund, a construction fund, and a debt-service reserve fund).133 Each of these funds is restricted by the terms of the bond documents under which the revenue bonds are issued. An issuer will commonly agree that a third-party trustee will maintain the proceeds of the revenue bonds and will disburse the proceeds of those bonds only upon the issuer’s submission of proper documentation (e.g., relevant evidence of construction pay applications).134

Bond Issuance Process

The procedures required to issue revenue bonds under North Carolina law are much less extensive than those required to issue general obligation (GO) bonds. Other than securing Local Government Commission (LGC) approval and adopting a bond order at the proper time, state law imposes few procedural requirements upon a local government’s issuance of revenue bonds.

LGC Approval

Although a unit of local government need not obtain voter approval to issue revenue bonds,135 it must obtain approval from the LGC to issue revenue bonds.

Application Process

A unit of local government seeking to issue revenue bonds must submit an application for approval to the LGC.136 And, as with GO bonds, the LGC may require the unit’s staff to meet with LGC staff prior to the acceptance of the application.137 Once the LGC accepts the unit’s application, it will consider whether to approve the proposed revenue bond issuance, and in doing so may consider, among other things, whether the probable net revenues of the financed assets will be sufficient to meet the debt service on the proposed revenue bonds.138

The LGC must approve a revenue bond issuance if it finds and determines all of the following:

The proposed revenue bond issue is necessary or expedient.

The amount proposed is adequate and not excessive for the proposed purpose of the issue.

The proposed project is feasible.

The unit’s debt-management procedures and policies are good or reasonable assurances have been given that its debt will henceforth be managed in strict compliance with law.

The increase in taxes, if any, necessary to service the proposed debt will not be excessive.

The proposed bonds can be marketed at reasonable interest cost.139

Ordinarily, the LGC will consider the approval of a unit’s application to issue revenue bonds at its regular monthly meeting.

Negotiating the Terms of a Revenue Bond Issuance

Revenue bonds are typically sold by negotiation rather than competitive bid, and a borrowing government typically selects an underwriter or placement agent at the outset of the negotiating process.140 The terms of the bonds—in particular, the terms of an issuer’s covenants—are negotiated over a series of weeks or months by representatives of an issuing local government, its regular counsel, bond counsel, one or more underwriters or placement agents and their counsel, staff members of the LGC, and, in some cases, the financial advisor to the issuing local government.

Adoption of Bond Order

With input from all of these stakeholders, bond counsel typically reduces the relevant terms to a bond order. As is the case for GO bonds, the bond order is the central document that a governing board must approve prior to issuing revenue bonds. It will, in comprehensive detail, set out the amount and purpose of the borrowing, the security for the revenue bonds issued, and the covenants to which the local government has agreed.141

Unlike with GO bonds, a unit’s governing board may introduce a bond order for revenue bonds at any regular or special meeting and adopt it at the same meeting, as long as the unit has submitted its application for approval to the LGC.142 To approve a revenue bond issuance, state law does not require the unit to publish notice of a referendum or take any other procedural action other than approving the bond order.

Issuance of the Bonds

The LGC sells revenue bonds on behalf of a unit of local government, typically on a negotiated basis.143 The date of sale is fixed by consultation with the LGC, the issuing unit of local government, its underwriter, and other parties involved in the transaction.144

Special Obligation Bonds

Security and Authority

North Carolina law authorizes certain units of local government to issue “special obligation” bonds for a limited number of purposes.145 In particular, counties, municipalities, and regional solid waste management authorities may issue special obligation bonds for solid waste management projects; certain water supply, conservation, and reuse projects; and wastewater collection and treatment projects.146 Municipalities also may issue special obligation bonds to finance or refinance projects that they may otherwise undertake in a municipal service district.147